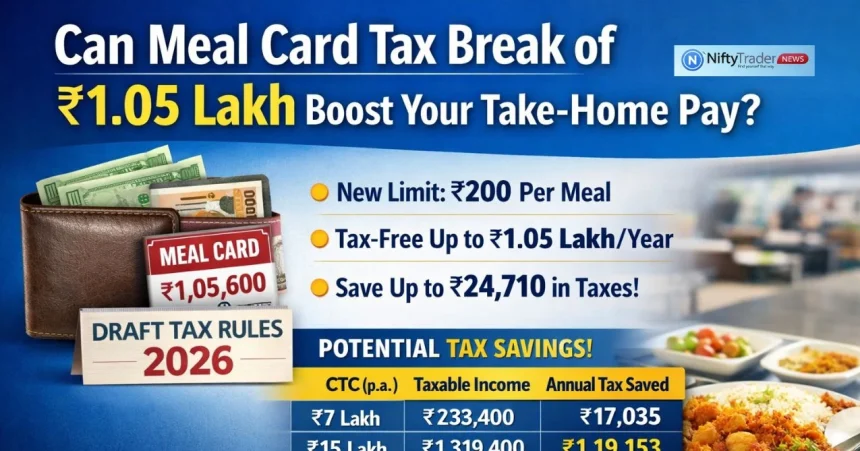

Under Draft Income‑Tax Rules, 2026, salaried workers in India could soon claim up to ₹1,05,600 per year in tax‑exempt meal‑card benefits, nearly 4× the current ₹26,400 limit if Parliament approves the changes ahead of the FY27 Budget. Experts estimate this could reduce taxable income by ₹79,200 and cut tax bills by as much as ~₹24,710 for those in the 30% slab, boosting take‑home pay significantly without raising direct salaries.

WHAT’S CHANGED: MEAL BENEFITS IN DRAFT RULES

🔹 New Perquisite Cap Raised

-

Draft rules propose a ₹200 per meal tax exemption, up from ₹50.

-

Assuming 2 meals/day × 22 working days × 12 months → ₹1,05,600 total yearly exemption.

🔹 How Exemption Works (Example)

-

₹200 × 2 meals/day = ₹400/day

-

₹400 × 22 working days = ₹8,800/month

-

₹8,800 × 12 months = ₹1,05,600/year.

REAL‑WORLD TAX IMPACT

(Under Old Regime + Standard Deduction ₹75,000)

| CTC | Taxable Income Before Meal Break | Taxable After Meal Exemption | Approx. Tax Savings |

|---|---|---|---|

| ₹7L | ₹594,400 | ₹519,400 | ₹17,035 |

| ₹13L | ₹1,194,400 | ₹1,119,400 | ₹87,953 |

| ₹15L | ₹1,394,400 | ₹1,319,400 | ₹119,153 |

| ₹20L | ₹1,894,400 | ₹1,819,400 | ₹180,253 |

| ₹25L | ₹2,394,400 | ₹2,319,400 | ₹208,853 |

(Figures reflect old regime; new regime outcomes vary due to structure differences.)

Incremental benefit (vs current ₹26,400 cap):

→ ~₹79,200 more exempt income annually

→ ~₹24,710 potential tax savings at 30% slab (incl. cess).

HOW IT WORKS—PERQUISITE VALUATION

Under the draft:

-

Meal vouchers (e.g., Sodexo/Pluxxee/Zaggle) provided at the workplace or redeemable at eating outlets remain tax‑free up to ₹200/meal.

-

Exemption also applies to free food/non‑alcoholic drinks provided during office hours, subject to conditions.

Gaurav Jain (Direct Tax Partner) clarifies that the value of the employer’s expenditure, net of employee contribution, determines the taxable perquisite value.

DOES THIS APPLY TO BOTH TAX REGIMES?

Old Regime:

The meal voucher break applies as per draft if approved.

New Regime:

Traditional exemptions are often excluded, so final treatment under the new regime remains uncertain pending legislative drafting.

This distinction matters: taxpayers under the new tax regime may not benefit unless Parliament explicitly includes perquisites in the exemption list.

WHY THIS MATTERS TO SALARIED TAXPAYERS

✔ Higher take‑home salary even without CTC increase

✔ Encourages structured employee benefits vs cash pay

✔ More relief for mid- to high-income tax brackets

✔ Alters old vs new regime calculus for some taxpayers

Given this scale, financial planners and HR teams are evaluating meal card optimization as a tax‑efficient compensation lever ahead of Budget 2026.

EXPERT INSIGHT

Dr. Raj P. Narayanam (Zaggle) calls this move a push toward “structured and transparent benefits ecosystems,” enabling employers to enhance employee take‑home value without proportionate cost increases.

BOTTOM LINE

Salaried taxpayers should:

-

Factor in the ₹1.05L meal exemption when planning your annual tax strategy (old regime).

-

Re‑evaluate the choice of tax regime if perquisites materially affect liability.

-

Coordinate with HR to structure meal benefits effectively to maximize exemptions.

Investors & compensation strategists should:

-

Monitor passage of rules; the interim draft may change before the Finance Act enactment.

-

Anticipate an employer shift toward non‑cash salary perks as an efficient cost strategy.

FREQUENTLY ASKED QUESTIONS

Q1: Who can claim the ₹1.05 lakh meal-card exemption?

A: Salaried employees receiving meal vouchers or cards from their employers can claim the exemption under Draft Income-Tax Rules 2026. Self-employed individuals are not eligible.

Q2: How is the exemption calculated?

A: The draft rule allows ₹200 per meal × 2 meals/day × ~22 working days/month × 12 months = ₹1,05,600 per year. Tax savings depend on your income slab (up to ~₹24,710 for 30% tax bracket).

Q3: Does it apply to both old and new tax regimes?

A: Currently, the exemption is explicitly structured for the old regime. Inclusion in the new regime depends on final legislative approval.

Q4: Are only cashless meal cards eligible?

A: No. Both cashless cards (Sodexo, Pluxxee, Zaggle) and employer-provided meals during work hours qualify, subject to ₹200 per meal limit.

Q5: How does this affect take-home salary?

A: By reducing taxable income, your take-home pay increases without any additional salary. Mid- to high-income employees benefit the most.

Q6: When will this rule come into effect?

A: The draft is under review. Once approved, it could take effect from FY27 (April 2026 onwards), subject to Finance Act enactment.