From pledging gold in a crisis to storing it under sovereign lock, three decades of inertia reversed in two years

The Numbers Behind the Move

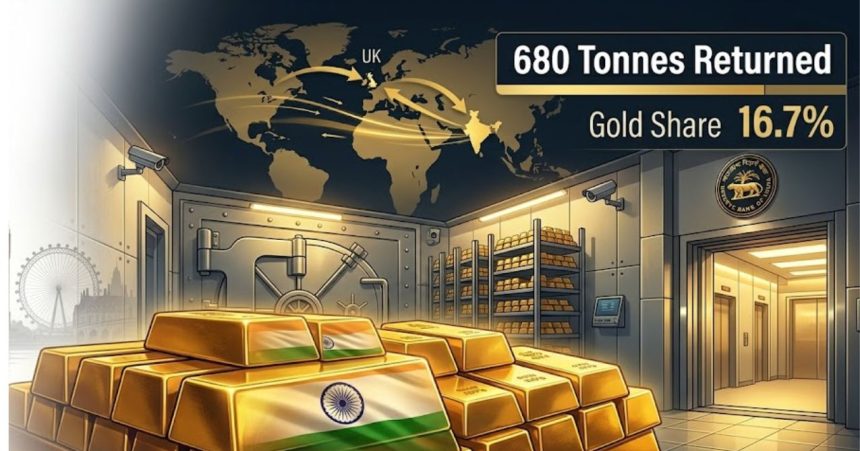

India has brought home 680.05 metric tonnes of its gold reserves as of end-March 2026, the Reserve Bank of India confirmed in its latest reserve management report. The RBI held 880.52 metric tonnes of gold in total as of end-March 2026, of which 680.05 metric tonnes were stored domestically, per RBI data. That flips the storage balance completely, as of March 2024, less than half of the gold reserves were held domestically, per the same RBI series. In two years, India went from minority domestic holder to storing more than 77% of its gold inside its own borders. That is not an incremental adjustment. That is a structural decision.

How Much Has Come Back, and How Fast

From March 2023 to September 2025, India repatriated almost 274 tonnes of gold, including more than 64 tonnes in just six months of FY26, per RBI data. Then the pace accelerated further. The RBI’s total gold holdings rose from 575.8 MT in September 2025 to 680 MT by end-March 2026, an addition of 104.2 MT in just six months, per RBI data. Gold stored overseas, mainly with the Bank for International Settlements, fell from 290.4 MT to 197.7 MT over the same period, per RBI data.

The pace of this repatriation has no modern Indian precedent outside the 1991 crisis. And that comparison matters precisely because 1991 was a crisis, and this is not. For further context: Germany’s Bundesbank took seven full years, from 2013 to 2020, to repatriate 674 tonnes from the US Federal Reserve and the Bank of France. India moved 280 tonnes in roughly two years. That is a significantly faster operational tempo for a repatriation of this scale.

What 1991 Has to Do With 2026

During the 1990-91 foreign exchange crisis, India pledged part of its gold reserves to the Bank of England to secure a $405 million emergency loan, per RBI historical records. The loan was repaid by November 1991, but the RBI kept the gold in London for logistical reasons; domestic vault infrastructure at the time was not certified to the international standards required for large-scale sovereign gold storage. That arrangement persisted quietly for more than three decades.

What changed was not just geopolitics. By 2022 to 2023, the RBI had upgraded its domestic vault facilities, in Nagpur and Mumbai—to LBMA-equivalent security and handling standards, removing the operational constraint that had kept the gold abroad in the first place. The Russian asset freeze in February 2022, when Western governments immobilised over $300 billion in Russian central bank reserves within days, then provided the strategic urgency. The domestic infrastructure was ready; the geopolitical case was now undeniable.

The Gold Share Number That Matters

India’s total foreign exchange reserves fell to $691.11 billion as of end-March 2026 from $700.09 billion six months earlier, per RBI data. Despite shrinking total reserves, gold’s weight inside that portfolio has risen sharply, from 13.9% to 16.7% between September 2025 and March 2026, per RBI data, reflecting both higher global gold prices and active accumulation.

Kotak Mahindra Asset Management and Nuvama Wealth Management analysts project India’s gold share could reach 20% by FY28 if accumulation continues at the current pace, a market inference, not a stated RBI policy target. At $691 billion in total reserves and current gold prices near $3,200 per troy ounce, a 20% gold share would imply approximately 1,340 tonnes of total gold holdings. India currently holds 880.52 tonnes. Reaching that level would require accumulating or repatriating roughly a further 460 tonnes, nearly double what was brought home in the last two years. That is the scale of ambition the trajectory implies, if the analysts are right.

That trajectory also matters in the context of reserve vulnerability. The ratio of volatile capital flows to reserves rose to 69.1% at end-December 2025 from 66.1% at end-September, while the ratio of short-term debt to reserves increased to 21.9% from 19.7%, per RBI data. More volatile liabilities against a shrinking reserve base is precisely the environment where hard assets with zero counterparty risk become more valuable, not less.

India Is Not Alone But It Is Moving Faster

Countries including China, Turkey, Russia, Poland, and several other emerging markets have increased gold purchases to record levels. Global central banks bought almost 415 tonnes in the first half of 2025, per World Gold Council data. What distinguishes India is not just the buying, it is the repatriation itself. Most central banks purchasing gold are content to store it in London or New York for liquidity convenience. India is explicitly pulling it home at pace.

The Cost Argument Nobody Mentions

There is a fiscal dimension to this that receives far less coverage than the sovereignty angle. Repatriation eliminates annual custody fees paid to the Bank of England. While the Bank of England does not publicly disclose its fee schedule, market estimates for central bank gold storage typically run at 10 to 15 basis points annually on the value stored. At current gold prices, India’s 680 tonnes of domestically held gold, had it remained in London, would represent a storage value of approximately $70 billion, implying annual custody costs in the range of $70 to $105 million. That is a recurring saving, every year, from this point forward.

Beyond cost, the RBI can now use domestically held gold to help manage local bullion prices, relevant given that gold ETF assets under management surged 191% in FY26, per AMFI data, creating a domestic gold market of a scale that gives the RBI new price-management instruments it simply did not possess when the bullion was sitting in London vaults. That policy optionality is new and underappreciated.

Also Read: RBI Accelerates Repatriation of Gold Reserves; 64 Tons Brought Back in H1 FY25

FAQs

How much of India’s gold is still stored abroad?

As of end-March 2026, approximately 197.7 metric tonnes remain stored overseas, primarily with the Bank for International Settlements, down from 290.4 MT six months earlier, per RBI data. That is roughly 22% of total holdings, compared to more than 50% just two years ago.

Has gold’s share in India’s forex reserves actually grown, or is it just a price effect?

Both factors are at work. Gold’s share rose from 13.9% to 16.7% between September 2025 and March 2026, per RBI data. Part of that reflects higher global gold prices; bullion has risen sharply through the Strait of Hormuz crisis, but the RBI has also been actively accumulating, adding over 104 tonnes to total holdings in just the last six months. Price alone does not explain the magnitude of the shift.

What does India gain by storing gold domestically rather than in London?

Three concrete things: elimination of estimated $70–105 million in annual Bank of England custody fees at current gold values; faster operational access during a financial crisis or capital flow shock; and protection from the jurisdictional risk demonstrated in February 2022, when over $300 billion in Russian central bank assets were frozen by Western governments within days. The 1991 precedent, when India pledged gold to the Bank of England for a $405 million emergency loan, remains institutional memory at the RBI. The domestic infrastructure being LBMA-certified now means there is no logistical reason left to keep the gold abroad.

The next RBI Annual Report, typically released in May, will provide the first detailed breakdown of FY27 reserve composition, including whether the analyst-projected 20% gold share target is reflected in any internal guidance. That document is the next data point worth watching on this story.