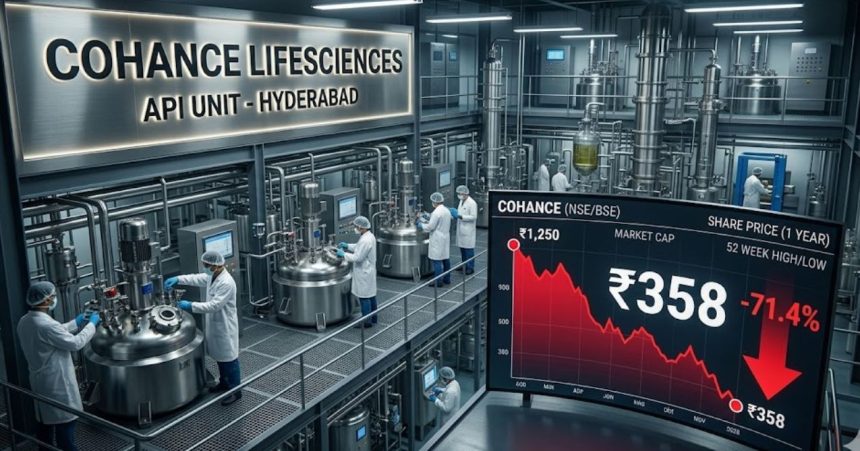

Shares of Cohance Lifesciences surged as much as 20% to Rs 432.10 on Monday, April 27, 2026, after the company announced the appointment of former Cipla Group CEO Umang Vohra as Executive Chairman and Group CEO, a leadership signal strong enough to recover nearly half the stock’s entire 2026 loss in a single trading session. Before Monday’s rally, Cohance was the third-worst performer on the Nifty Smallcap index year-to-date with losses of 31%. The stock remains down 20% for 2026 even after the surge.

What Destroyed the Stock: Three Simultaneous Hits

The collapse is not a single-cause story. Q3 FY26 revenue fell 19.5% year-on-year to ₹545 crore, while the nine-month FY26 revenue declined 6.7% to ₹1,650 crore. Three factors drove this simultaneously:

First, destocking in two large commercial products accounted for approximately ₹260 crore in revenue loss as customers normalised inventories. Second, EBITDA dropped 60% year-on-year in Q3 FY26 to Rs 968 million, with EBITDA margins collapsing to 17.5% from 35% in Q3 FY25. Net profit for Q3 FY26 fell 76% to Rs 367 million compared to Rs 1,530 million in the same period last year.

Third and most structurally damaging, Cohance’s Nacharam formulation facility received a US FDA Warning Letter following an Official Action Indicated (OAI) classification after an inspection conducted from August 4–12, 2025. The Warning Letter directly impacted export capabilities to regulated markets. Remediation is underway, and non-US market production has resumed, but the facility’s full clearance timeline has not been disclosed. Management on the Q3 concall (February 12, 2026) characterised FY26 as a “transition year” due to product timing, customer delays, and patent expiries, while stressing these are not structural issues and reaffirming FY27 growth expectations.

The Promoter Pledge Problem

A fourth risk sits outside operations entirely. 100% of promoter shares in Cohance Lifesciences are pledged. In a stock that has already fallen sharply, a full promoter pledge is a forced-seller risk: any margin call triggered by further price decline could result in automatic block sales, amplifying downward momentum independent of business performance. Promoter holding has declined from 66.41% in June 2025 to 57.49% as of Q3 FY26, while FII holding fell from 11.05% in March 2025 to 6.02% by December 2025, a 499 basis point exit by foreign institutional investors over nine months.

Who Is Umang Vohra and Why Does the Appointment Matter

Vohra spent over three decades at Cipla, serving as its Managing Director and Group CEO until he stepped down in October last year, completing his notice period on March 31, 2026, with Achin Gupta named as his successor. He brings a track record of scaling complex, multi-geography pharmaceutical businesses—precisely what Cohance needs given its current revenue base of ₹1,650 crore for the first nine months of FY26.

The BSE filing dated April 27, 2026, states that Vohra’s appointment reflects a deliberate, strategic decision by the board to bring in a leader whose profile is specifically suited to the demands of the company’s next phase. Outgoing Executive Chairman Vivek Sharma, who oversaw the merger of Cohance with Suven Pharmaceuticals, completed May 1, 2025, will remain as a Special Advisor for nine months to ensure continuity.

The honest tension here: Vohra built his career scaling a branded generics and over-the-counter business. Cohance is a pure-play science-led CDMO serving global innovators. The commercial muscle he brings is real. Whether his specific playbook, US market breadth, geographic diversification, consumer brand building transfer to a CDMO model built on molecular complexity, Phase III pipelines, and ADC manufacturing is the question the market will spend the next 12 months answering. Cohance is currently supporting nine Phase III molecules, with four expected to transition to commercial supply over the next 12–18 months. Vohra’s ability to accelerate those conversions is the metric that matters most.

What Would Recovery Actually Look Like

Management has reiterated a mid-term EBITDA margin guidance of 30%+, characterising current margin pressure as timing-related rather than structural. The company generated positive free cash flow of ₹175 crore during the first nine months of FY26 despite the revenue slump, with capital expenditure of ₹161 crore evidence of operational cash discipline even under severe stress. The long-term $1 billion revenue target remains on the company’s roadmap, though management acknowledged in the Q3 conference call that timing may shift slightly due to current year challenges.

Monday’s 20% surge is a meaningful signal. It is not yet a catalyst.

Also Read: Sitharaman: AI Cyberattacks Are India’s Gravest Market Threat

FAQ

What caused Cohance Lifesciences’ stock to fall so sharply in 2026?

Three simultaneous hits: a ₹260 crore destocking impact from two large commercial products, a US FDA Warning Letter for the Nacharam facility issued in August 2025, and Q3 FY26 net profit collapsing 76% year-on-year to Rs 367 million. EBITDA margins fell from 35% to 17.5% over the same period. The stock was the third-worst YTD performer on the Nifty Smallcap index, down 31% before Monday’s rally.

Who is Umang Vohra, and what is his background?

Umang Vohra is the former Managing Director and Group CEO of Cipla Limited. He stepped down from Cipla in October last year and completed his notice period on March 31, 2026, with Achin Gupta succeeding him. He takes over as Cohance’s Executive Chairman on May 1, 2026, and Group CEO on May 20, 2026.

Is the FDA Warning Letter for Cohance’s Nacharam facility resolved?

Not fully. As of April 27, 2026, remediation actions are underway, and non-US market production has resumed. The full clearance timeline for US market exports has not been publicly disclosed by the company.

Are Cohance promoter shares fully pledged?

Yes. As of the latest available data, 100% of promoter shares are pledged. This creates a forced-seller risk: any margin call triggered by further price declines could result in automatic block sales that amplify downward price pressure regardless of business performance.

What is Cohance Lifesciences’ revenue target, and when will it reach $1 billion?

Cohance has stated a long-term target of $1 billion in revenue. Management acknowledged in the Q3 FY26 concall (February 12, 2026) that the timeline may shift slightly due to FY26 challenges. No specific year has been confirmed. FY27 is expected to see a return to growth, with four of the company’s nine Phase III molecules expected to move to commercial supply in the next 12–18 months.