Key Takeaways

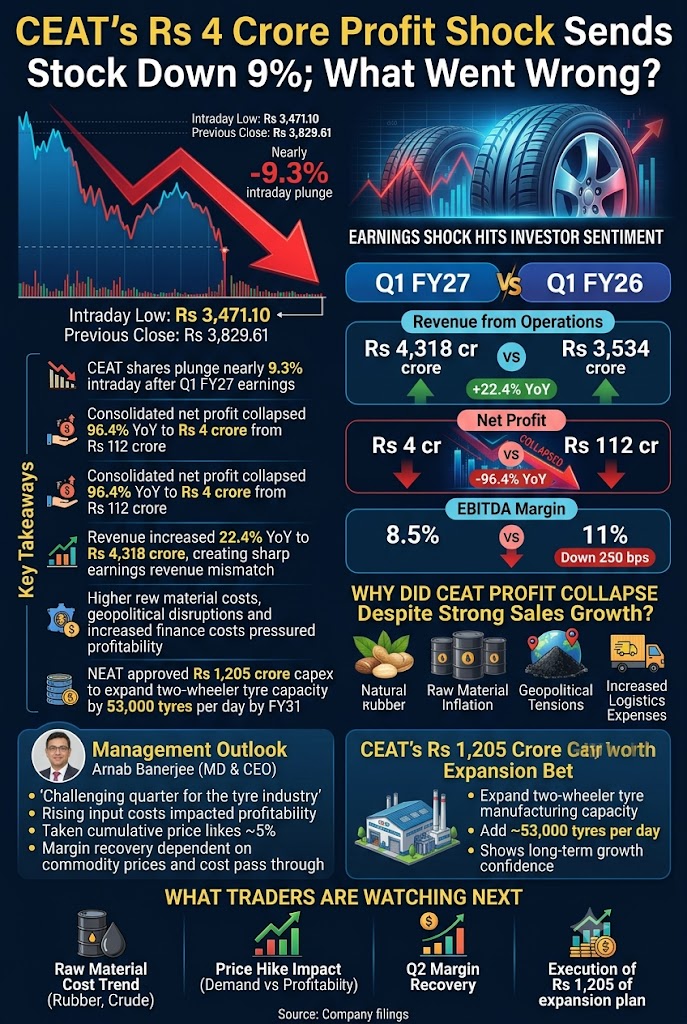

- CEAT shares plunged nearly 9.3% intraday after Q1 FY27 earnings triggered heavy selling.

- Consolidated net profit collapsed 96.4% YoY to Rs 4 crore from Rs 112 crore.

- Revenue increased 22.4% YoY to Rs 4,318 crore, creating a sharp earnings-revenue mismatch.

- Higher raw material costs, geopolitical disruptions and increased finance costs pressured profitability.

- CEAT approved Rs 1,205 crore capex to expand two-wheeler tyre capacity by 53,000 tyres per day by FY31.

- The near-term stock direction depends on whether price hikes can offset continued margin pressure.

CEAT Shares Slide After Earnings Shock Hits Investor Sentiment

CEAT shares came under intense selling pressure on Friday after the tyre manufacturer reported a sharp collapse in quarterly profitability. The stock fell as much as 9.3% to Rs 3,471.10 on NSE, before recovering partially to trade near Rs 3,550.

The market reaction was driven by a major earnings mismatch, CEAT delivered strong revenue growth, but almost lost its entire quarterly profit.

While sales increased more than 22%, investors focused on the sharp erosion in margins and questioned how quickly profitability can recover amid elevated input costs.

The stock’s fall highlights a key market lesson: strong topline growth is not enough when earnings quality deteriorates.

CEAT Q1 FY27 Results: Revenue Rises, Profit Nearly Disappears

| Particulars | Q1 FY27 | Q1 FY26 | YoY Change |

|---|---|---|---|

| Revenue from Operations | Rs 4,318 crore | Rs 3,534 crore | +22.4% |

| Net Profit | Rs 4 crore | Rs 112 crore | -96.4% |

| EBITDA | Rs 365 crore | Rs 387 crore | -5.7% |

| EBITDA Margin | 8.5% | 11% | Down 250 bps |

Source: Company filings

The numbers reveal the biggest concern for investors, demand remained healthy, but profitability weakened sharply.

Why Did CEAT Profit Collapse Despite Strong Sales Growth?

The biggest surprise in CEAT’s Q1 results was not weak demand. It was the speed at which costs consumed profitability.

Tyre manufacturers are highly sensitive to:

- Natural rubber prices

- Carbon black costs

- Crude-linked raw materials

- Logistics expenses

During the quarter, higher input costs linked to geopolitical tensions, including the West Asia situation, increased pressure on margins.

CEAT attempted to offset the impact through price increases, but the benefit was not enough to fully protect earnings.

The result:

Revenue growth continued, but profit almost vanished.

This expectation gap between sales performance and profitability was the primary reason behind the sharp stock reaction.

Hidden Pressure: Finance Costs Added to Margin Pain

While raw material inflation was the biggest challenge, the earnings disappointment was also linked to higher financial costs.

Broker commentary indicated that operational performance was relatively stable, but higher interest and finance expenses added further pressure on the bottom line.

This means the profit decline was not only a commodity-cost issue but also a balance-sheet pressure story.

Management Outlook: Margin Recovery Still Uncertain

CEAT MD and CEO Arnab Banerjee called Q1 a challenging quarter for the tyre industry as rising input costs impacted profitability.

The company has already taken cumulative price hikes of around 5% and plans to maintain pricing discipline while protecting demand.

However, management indicated that raw material costs could remain elevated in Q2, making margin recovery dependent on:

- Further commodity price movement

- Ability to pass costs to customers

- Demand stability after price hikes

The biggest risk for investors is that continued inflation could delay earnings recovery.

CEAT’s Rs 1,205 Crore Expansion Bet

Despite the near-term earnings pressure, CEAT continues to invest for long-term growth.

The company’s board approved a Rs 1,205 crore investment plan to expand two-wheeler tyre manufacturing capacity.

The expansion will add approximately:

53,000 tyres per day capacity by FY31

The move shows management’s confidence in long-term demand growth, especially in the two-wheeler segment.

However, investors will watch whether this expansion delivers better returns once margins stabilise.

CEAT Stock Performance and Analyst View

| Parameter | Value |

|---|---|

| Intraday Low | Rs 3,471.10 |

| Previous Close | Rs 3,829.61 |

| Market Reaction | Down over 9% |

| Market Capitalisation | Around Rs 14,346 crore |

| 1-Month Return | Nearly -10% |

| 5-Year Return | Around +145% |

Despite the weak quarter, some brokerages remain positive on CEAT’s long-term prospects.

Motilal Oswal retained its Buy view, citing long-term growth potential and valuing the stock at:

- 25.2x FY27E earnings

- 16.3x FY28E earnings

However, analyst opinion remains mixed, reflecting uncertainty around the pace of margin recovery.

What Traders Are Watching Next

1. Raw Material Cost Trend

Any cooling in rubber and crude-linked input prices could improve margins.

2. Price Hike Impact

Investors will track whether higher prices hurt demand or successfully restore profitability.

3. Q2 Margin Recovery

The next earnings quarter will be crucial to determine whether Q1 was a temporary pressure phase or the beginning of a longer margin challenge.

4. Two-Wheeler Capacity Expansion

Execution of the Rs 1,205 crore investment plan will remain a long-term growth trigger.

Read Next: Adani, Groww Among 12 Stocks in Focus Ahead of MSCI Review

Final Take

CEAT’s Q1 FY27 results created a classic market conflict, strong revenue growth but collapsing profitability.

The stock reaction shows investors are currently prioritising earnings visibility over sales momentum.

The company’s long-term expansion strategy remains intact, but near-term performance will depend heavily on commodity prices, pricing power and margin recovery.

For traders, the key trigger is not revenue growth anymore, it is whether CEAT can rebuild profitability in the next few quarters.