Key Takeaways

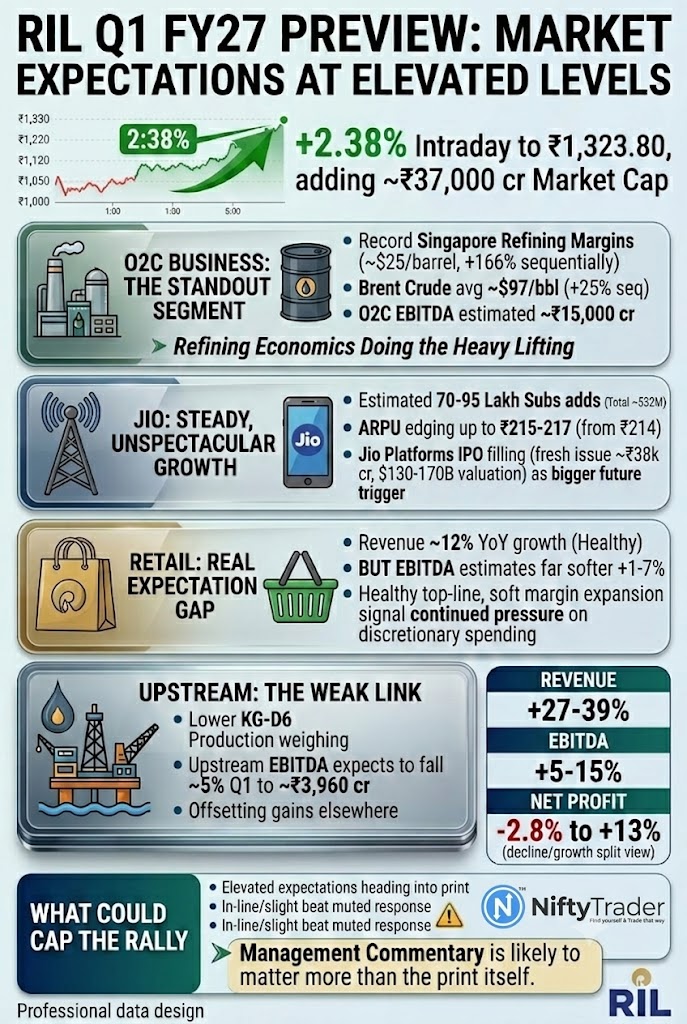

- RIL shares gained as much as 2.38% intraday to ₹1,323.80, adding close to ₹37,000 crore in market cap ahead of today’s Q1 FY27 print

- Street estimates put revenue growth at 27-39% YoY and EBITDA growth at 5-15% YoY, but net profit views range from a 2.8% decline to 13% growth

- Record Singapore refining margins (~$25/barrel, +166% sequentially) make O2C the standout segment this quarter

- Retail shows a real expectation gap: revenue growth near 12% YoY, but EBITDA growth estimates are far softer at 1-7%

- Jio should add 70-95 lakh subscribers, with ARPU edging up to ₹215-217 from ₹214

- Elevated expectations mean even an in-line beat could trigger a muted stock reaction; management commentary is likely to matter more than the print itself

Reliance Industries Ltd, one of India’s most valuable listed companies and among the heaviest weights in the Nifty 50, will report Q1 FY27 earnings after market hours today. The stock climbed as much as 2.38% intraday to ₹1,323.80, adding roughly ₹37,000 crore to its market capitalisation, as brokerages head into the print broadly constructive, though how that optimism splits across segments varies a lot depending on whose model you read.

O2C Business Leads The Charge

Refining economics did the heavy lifting this quarter. Singapore Gross Refining Margins hit a record near $25 a barrel, up 166% sequentially on strong distillate cracks, per an Equirus Securities sector note, while Brent crude averaged around $97 a barrel, up 25% sequentially.

ICICI Securities estimates O2C EBITDA at ₹15,000 crore (+3% QoQ); Emkay Global pegs it slightly lower at ₹14,800 crore (+2% QoQ). Either way, O2C looks set to be the single biggest swing factor in the quarter.

Jio Holds Steady

Jio is expected to add between 70 lakh and 95 lakh subscribers, taking its base to roughly 531-532 million, with ARPU inching up to ₹215-217 from ₹214 in the March quarter, per ICICI Securities and Nomura.

A separate Business Standard–compiled estimate puts Jio’s revenue growth at 10.9% YoY to ₹34,236 crore and EBITDA growth at 11.7% YoY to ₹18,650 crore, with margins improving to 54.5%.

Beyond the quarter, the bigger trigger may be the Jio Platforms IPO: the unit filed its draft prospectus with SEBI on June 19, targeting a fresh issue of about ₹38,000 crore, with bankers valuing it between $130 billion and $170 billion.

Retail’s Real Expectation Gap

This is where Doc 93’s framing was right but under-supported. Reliance Retail’s revenue is estimated to grow around 12% year-on-year, per Nomura, but EBITDA growth looks far more modest across brokerage models: Nomura sees +3% YoY to ₹6,600 crore, ICICI Securities +7% YoY to ₹6,830 crore, and Emkay Global +1% QoQ to ₹6,990 crore. Healthy top-line growth paired with soft margin expansion points to continued pressure on discretionary spending.

Upstream Stays The Weak Link

Lower KG-D6 production continues to weigh on the oil and gas business. Emkay Global expects upstream EBITDA to fall 5% QoQ to ₹3,960 crore, partly offsetting gains elsewhere.

| Brokerage | Revenue (YoY) | EBITDA (YoY) | Net Profit (YoY) |

|---|---|---|---|

| Equirus Securities | ₹3.28 lakh cr (+35%) | ₹49,100 cr (+14.5%) | ₹24,593 cr (+13%) |

| Emkay Global | ₹3.38 lakh cr (+38.9%) | ₹45,013 cr (+4.9%) | ₹17,567 cr (-2.8%) |

| Street range* | ₹3.09-3.2 lakh cr | ₹47,100-49,100 cr | ₹16,200-18,470 cr |

*Aggregate brokerage poll. Source: Business Standard (July 16, 2026); BusinessToday brokerage tracker.

Track how institutional money is positioned ahead of the print on NiftyTrader’s FII-DII Tracker.

| Stock | Key Trigger | Trader View |

|---|---|---|

| Reliance Industries | Q1 FY27 results and management commentary due post-market hours today | Stock has ranged roughly ₹1,290-1,324 intraday; volatility likely on O2C margin, retail EBITDA and Jio ARPU cues |

Check Live: Reliance Option Chain Live – RIL Options Data

What Could Cap The Rally

Expectations are already elevated heading into the print, which cuts both ways. An in-line or even slightly better-than-expected result could still trigger a muted reaction if it merely meets what’s already priced in, while any caution on refining margin sustainability, retail demand, or capex could prompt profit-booking after today’s pre-results move.

Bottom Line

RIL heads into its Q1 FY27 print near its day’s high, with O2C poised to be the standout and Jio delivering steady, unspectacular growth. The real split among brokerages is on the bottom line, some see double-digit profit growth, others a decline, driven by how each models margin pressure from crude costs and a weaker rupee.

With expectations this elevated, tonight’s management commentary on refining sustainability, retail demand, and the Jio IPO timeline is likely to move the stock more than the headline numbers themselves.

Read Next: CEAT’s Rs 4 Crore Profit Shock Sends Stock Down 9%; What Went Wrong?

This article is for informational purposes only and should not be construed as investment advice. Please consult a SEBI-registered financial advisor before making investment decisions.