MCX Commodity Outlook: Why Gold, Silver and Crude Oil Could Stay Volatile Next Week

Will gold regain momentum, or will soaring crude oil prices keep metals under pressure? As tensions in the Gulf region intensify and the Federal Reserve remains cautious on interest rates, commodity markets are entering one of their most uncertain weeks this year. Here’s why traders and investors should closely watch every headline before making their next move.

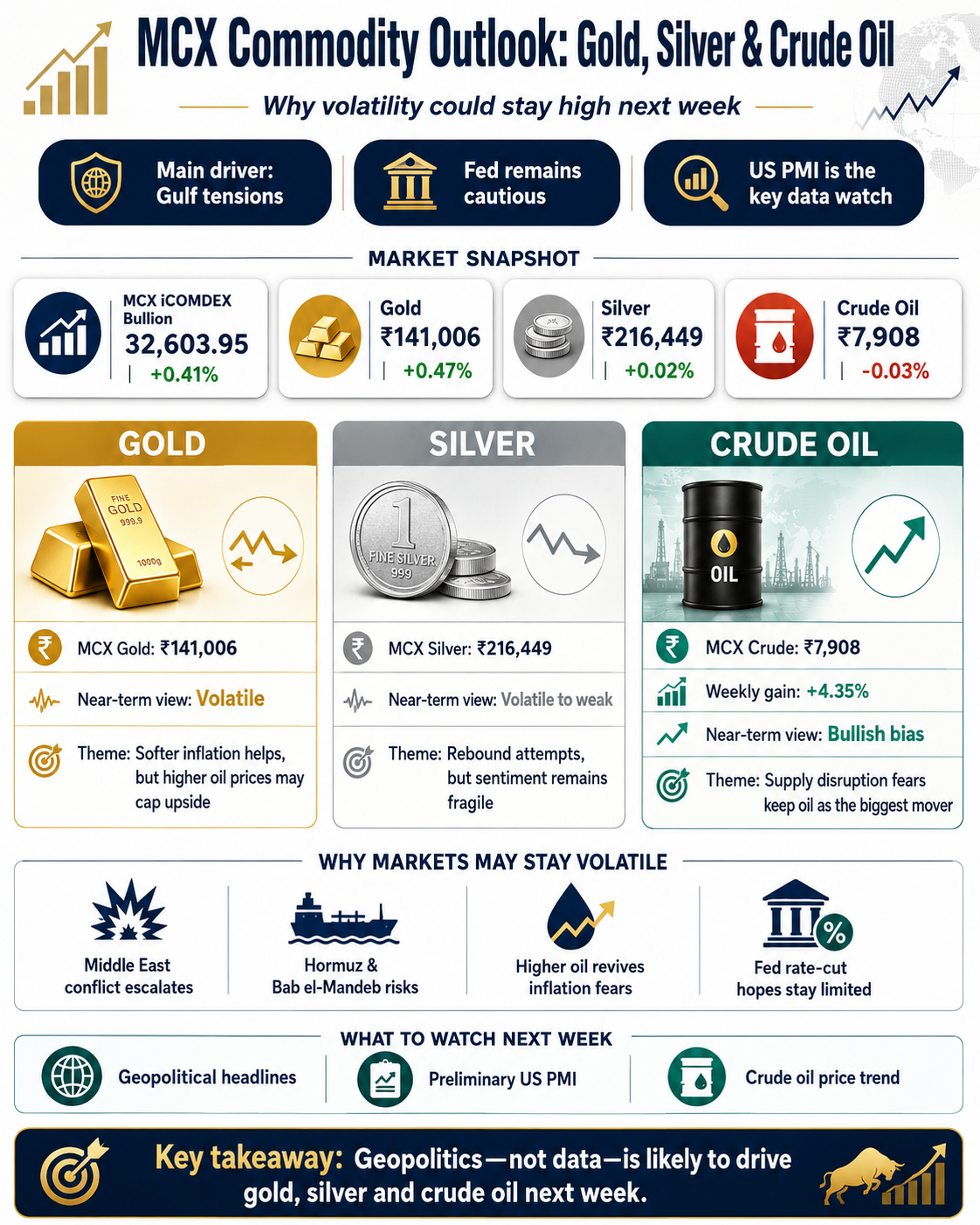

MCX Commodity Metals outlook next week hinges on Gulf conflict and Fed policy

The Metals Outlook Next Week is expected to remain highly volatile as geopolitical tensions overshadow economic data. While softer US inflation briefly supported market sentiment, renewed military action in the Middle East has once again shifted investor attention toward energy prices and inflation risks.

With only preliminary US PMI data scheduled next week, market participants are likely to react more to geopolitical headlines than economic releases.

Track Live : MULTI COMMODITY EXCHANGE OF INDIA

MCX iCOMDEX Indices

Selected Index: MCX iCOMDEX Bullion

Index Performance

- Index Value: 32,603.95

- Change: +0.41% ▲

Reference level shown on chart:

- 32,471.32

Time markers on chart:

- 9:30

- 13:30

- 17:30

- 21:30

Market Activity Time: 23:30 | 17 Jul 2026

| Commodity | Expiry | Price | Change |

|---|---|---|---|

| Gold | 05AUG2026 | 141006.00 | +0.47% |

| Copper | 31JUL2026 | 1303.70 | +0.10% |

| Silver | 04SEP2026 | 216449.00 | +0.02% |

| Crude Oil | 19AUG2026 | 7908.00 | -0.03% |

| Zinc | 31JUL2026 | 372.90 | -0.07% |

| Natural Gas | 28JUL2026 | 281.50 | -0.07% |

| Lead | 31JUL2026 | 198.75 | -0.13% |

| Cardamom | 31JUL2026 | 3375.00 | -0.53% |

Middle East tensions continue to drive commodity markets

The conflict escalated further after continued US strikes on Iranian military infrastructure and Iran’s retaliation against US-linked assets across the region.

Markets also remain concerned about possible disruptions at both the Strait of Hormuz and the Bab el-Mandeb Strait—two of the world’s most important energy shipping routes. Any disruption could tighten global oil supplies and fuel another surge in crude prices.

These developments have become the biggest driver of the Metals Outlook Next Week.

Read More : Reliance Posts Record Rs 23,196 Crore Profit in Q1 FY27, Jio IPO on the Horizon

Key takeaways

- Geopolitics remains the biggest market driver as military escalation in the Gulf continues and the peace framework has been suspended.

- US inflation cooled, with softer CPI and PPI supporting a patient Federal Reserve, although policymakers remain cautious about easing.

- Gold and silver weakened despite briefly benefiting from softer inflation, as higher oil prices revived inflation concerns and expectations of higher interest rates.

- Base metals were mixed. Aluminium remained relatively resilient due to supply concerns, while copper edged higher and zinc underperformed.

- Crude oil recorded its strongest weekly gain since April, supported by disruptions around the Strait of Hormuz and the growing risk of a second shipping chokepoint at Bab el-Mandeb.

- Outlook for next week: US economic data is limited, with preliminary PMI readings the main scheduled release. Commodity markets are expected to remain driven primarily by geopolitical developments rather than macroeconomic data.

Softer inflation offers relief, but the Fed stays cautious

US inflation cooled in June, with CPI easing to 3.8% from 4.2% in May. Lower gasoline prices helped slow inflation, while retail sales continued to show resilience.

However, Fed Chair Christopher Warsh maintained a cautious stance.

“The Federal Reserve remains committed to price stability despite improving inflation data.”

Comments from other Fed officials also reduced expectations of an early rate cut, keeping higher interest rate concerns alive.

MCX Top Gainers As on: 17 Jul 2026 | 23:30

| Rank | Commodity | Expiry | Close | LTP | Change | % Change |

|---|---|---|---|---|---|---|

| 1 | GOLD | 05AUG2026 | 140348.00 | 141006.00 | +658.00 | +0.47% |

| 2 | CRUDEOILM | 19AUG2026 | 7906.00 | 7918.00 | +12.00 | +0.15% |

| 3 | COPPER | 31JUL2026 | 1302.35 | 1303.70 | +1.35 | +0.10% |

| 4 | SILVERMIC | 31AUG2026 | 219886.00 | 220100.00 | +214.00 | +0.10% |

| 5 | GOLDM | 05AUG2026 | 140782.00 | 140900.00 | +118.00 | +0.08% |

| 6 | GOLDGUINEA | 31JUL2026 | 113870.00 | 113960.00 | +90.00 | +0.08% |

| 7 | SILVERM | 31AUG2026 | 219825.00 | 219992.00 | +167.00 | +0.08% |

| 8 | NICKEL | 19AUG2026 | 1626.30 | 1627.30 | +1.00 | +0.06% |

| 9 | GOLDPETAL | 31JUL2026 | 14222.00 | 14230.00 | +8.00 | +0.06% |

| 10 | SILVER100 | 31JUL2026 | 2174.00 | 2175.00 | +1.00 | +0.05% |

MCX Top Losers As on: 17 Jul 2026 | 23:30

| Rank | Commodity | Expiry | Close | LTP | Change | % Change |

|---|---|---|---|---|---|---|

| 1 | CARDAMOM | 31JUL2026 | 3393.00 | 3375.00 | -18.00 | -0.53% |

| 2 | MENTHAOIL | 31JUL2026 | 1290.50 | 1287.00 | -3.50 | -0.27% |

| 3 | LEAD | 31JUL2026 | 199.00 | 198.75 | -0.25 | -0.13% |

| 4 | LEADMINI | 31JUL2026 | 199.00 | 198.85 | -0.15 | -0.08% |

| 5 | ZINC | 31JUL2026 | 373.15 | 372.90 | -0.25 | -0.07% |

| 6 | NATURALGAS | 28JUL2026 | 281.70 | 281.50 | -0.20 | -0.07% |

| 7 | NATGASMINI | 28JUL2026 | 281.80 | 281.60 | -0.20 | -0.07% |

| 8 | ALUMINI | 31JUL2026 | 343.25 | 343.10 | -0.15 | -0.04% |

| 9 | ELECDMBL | 30JUL2026 | 4698.00 | 4696.00 | -2.00 | -0.04% |

| 10 | CRUDEOIL | 19AUG2026 | 7910.00 | 7908.00 | -2.00 | -0.03% |

Gold and silver struggle as inflation fears return

Gold briefly benefited from softer inflation before renewed geopolitical tensions reversed gains.

Spot gold closed above $4,000 per ounce but still lost 2.5% during the week. Silver recovered from recent lows but finished more than 7% lower.

Higher energy prices could keep inflation elevated, limiting upside for precious metals in the near term.

Base metals deliver mixed performance

Industrial metals showed mixed trends.

Copper ended the week slightly higher around $13,525 per tonne, while zinc fell more than 2%. Aluminium remained relatively strong due to supply concerns, China’s production limits and falling LME inventories.

The Metals Outlook Next Week suggests industrial metals may remain highly sensitive to both crude oil prices and geopolitical developments.

Crude oil remains the biggest market mover

Crude oil delivered its strongest weekly rally since April.

Brent crude climbed nearly 15% to around $88.30 per barrel, while WTI rose to $82.70 as supply concerns intensified.

MCX Crude Oil futures ended at ₹7,945 per barrel, gaining 4.35% for the week. Technical indicators continue to favour bullish momentum unless geopolitical tensions ease.

Here’s what happened today and why traders reacted

Commodity traders reacted primarily to rising geopolitical risks rather than economic data.

Fresh military strikes, fears of supply disruptions and Iran’s suspension of its peace MOU pushed crude oil higher and revived inflation concerns. Although US inflation cooled, the Fed’s cautious outlook prevented investors from turning bullish on precious metals.

The combination of higher oil prices and policy uncertainty kept commodity markets volatile throughout the week.

What does the Metals Outlook Next Week mean for investors?

The Metals Outlook Next Week indicates that volatility is likely to remain elevated.

Higher crude prices could benefit energy producers but may pressure sectors such as aviation, paints, chemicals and transportation due to rising input costs.

Commodity traders should closely monitor developments in the Middle East, while investors should also watch preliminary US PMI data for fresh clues on global economic activity.

For now, geopolitical headlines—not economic reports—are expected to remain the biggest catalyst for metals, crude oil and broader commodity markets.