US Fed to Hold Rates, but Why GoalFi Founder Sees Higher Hike Risk Than Cuts in 2026

Will the US Federal Reserve finally start cutting interest rates, or could investors be underestimating the possibility of another hike? While markets expect policymakers to stay on hold this month, GoalFi Founder Robin Arya believes the bigger surprise could come in 2026. Here’s why he remains cautious on markets, bullish on healthcare and selective on long-term investments.

US Fed to hold rates as inflation remains above target

The Fed to Hold Rates narrative is expected to continue at the US Federal Reserve’s July 29 meeting as policymakers remain cautious about inflation.

Robin Arya, Founder and Managing Director of GoalFi, expects the Fed to leave the benchmark interest rate unchanged at 3.50%–3.75%, noting that US inflation remains close to 3.8%, well above the Fed’s 2% target.

“I would expect the Fed to stay unchanged on July 29. But for 2026, the risk is towards a hike and not a cut,” Arya said.

He believes inflation remains too high for policymakers to begin easing monetary policy.

RBI is also likely to remain on hold

Arya expects the Reserve Bank of India (RBI) to maintain its current policy stance as well.

The RBI recently retained a neutral stance while revising its inflation forecast higher to 5.1% and lowering GDP growth expectations to 6.6%.

Although inflation remains above the RBI’s 4% target, it is still within the central bank’s 2–6% tolerance band, making a wait-and-watch approach more likely.

“The combination of higher inflation and slower growth argues for patience rather than immediate rate cuts,” Arya noted.

Read More : MCX Commodity Outlook: Why Gold, Silver and Crude Oil Could Stay Volatile Next Week

Markets may remain volatile despite improving sentiment

Arya believes equity markets could continue witnessing sharp swings throughout the current quarter.

While better-than-expected IT sector earnings have helped the Nifty attempt to build a technical base, he believes broader market fundamentals remain mixed.

Large-cap earnings expectations remain muted, suggesting investors should focus on sector-specific stock selection instead of relying solely on benchmark indices.

Geopolitical tensions and elevated crude oil prices are also expected to keep volatility high.

Track Live : Nifty Open Interest (OI) Live

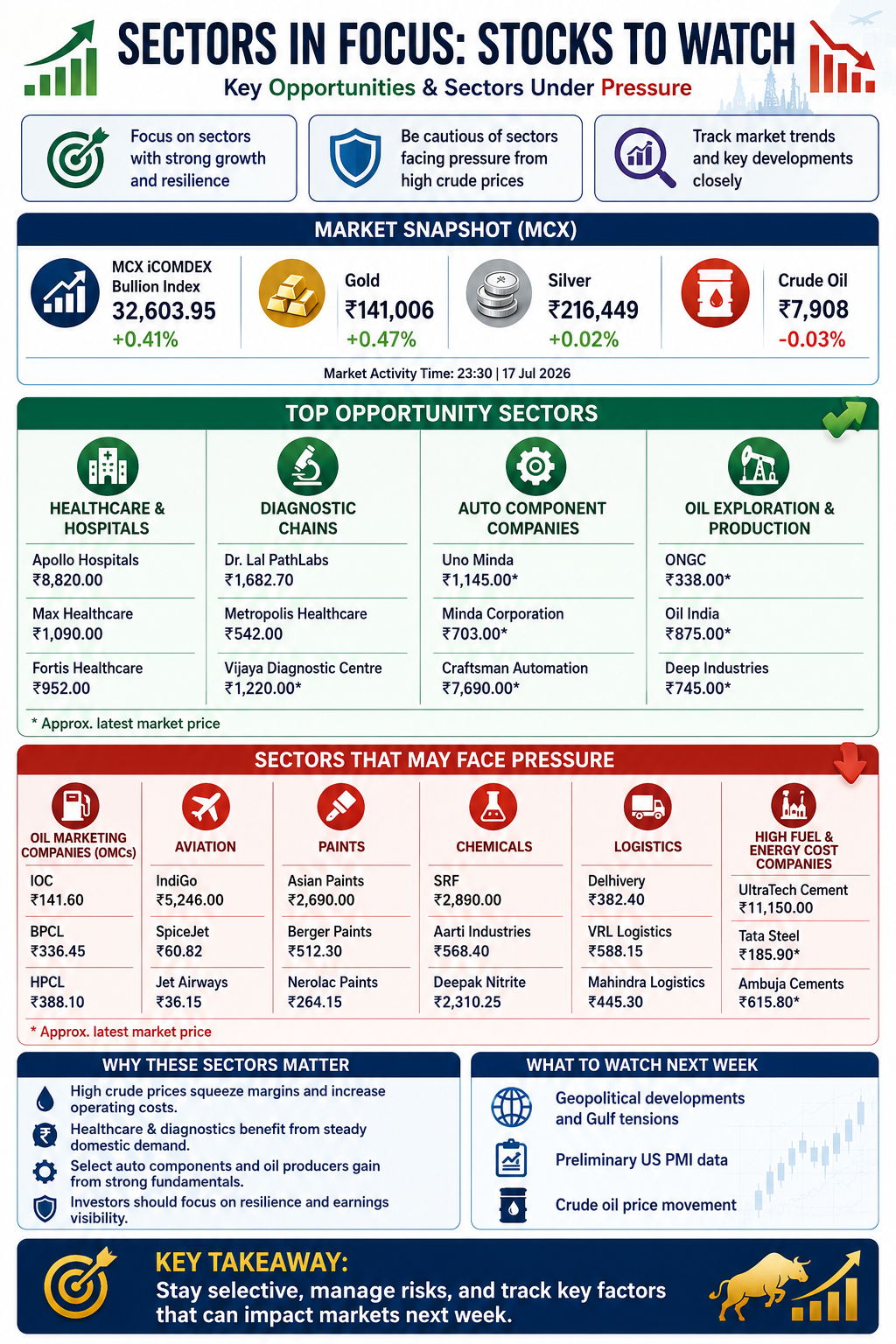

| Sectors | Company | NSE Symbol | Current Price |

|---|---|---|---|

| Healthcare & Hospitals | Apollo Hospitals Enterprise Ltd | APOLLOHOSP | ₹8826.00 |

| Max Healthcare Institute Ltd | MAXHEALTH | ₹1089.90 | |

| Fortis Healthcare Ltd | FORTIS | ₹952.45 | |

| Diagnostic Chains | Dr. Lal PathLabs Ltd | LALPATHLAB | ₹1687.40 |

| Metropolis Healthcare Ltd | METROPOLIS | ₹545.30 | |

| Vijaya Diagnostic Centre Ltd | VIJAYA | ₹1341.30 | |

| Auto Component Companies | Uno Minda Ltd | UNOMINDA | ₹1154.80 |

| Minda Corporation Ltd | MINDACORP | ₹678.30 | |

| Craftsman Automation Ltd | CRAFTSMAN | ₹9105.00 | |

| Oil Exploration & Production | Oil and Natural Gas Corporation Ltd | ONGC | ₹247.29 |

| Oil India Ltd | OIL | ₹435.35 | |

| Deep Industries Ltd | DEEPINDS | ₹476.00 |

Quick sector view

- Healthcare & Hospitals: Apollo Hospitals, Max Healthcare and Fortis Healthcare remain the leading listed hospital operators, supported by strong domestic healthcare demand.

- Diagnostics: Dr. Lal PathLabs, Metropolis Healthcare and Vijaya Diagnostic are among India’s leading organized diagnostic chains, benefiting from preventive healthcare and rising testing demand.

- Auto Components: Uno Minda, Minda Corporation and Craftsman Automation are key beneficiaries of domestic vehicle production and premiumisation.

- Oil & Gas: ONGC and Oil India generally benefit from higher crude prices due to improved realizations, while Deep Industries gains from increased upstream exploration and oilfield activity.

Note: The prices marked “approx.” are indicative latest market levels and may vary slightly depending on the exchange closing price or live market movements.

Healthcare emerges as the preferred investment theme

Among various sectors, Arya sees healthcare, hospitals and diagnostic chains offering the most attractive risk-reward opportunity.

Diagnostic companies continue guiding for 13–15% growth, supported by rising preventive healthcare and chronic disease monitoring.

Although hospital profitability remains under pressure due to capacity expansion, he believes the long-term earnings outlook remains healthy.

Healthcare also benefits from relatively limited exposure to global commodity prices and international economic uncertainty.

Track Live : Nifty PCR Today – Live Put Call Ratio Chart

| Sector | Company | NSE Symbol | Current Stock Price |

|---|---|---|---|

| Oil Marketing Companies (OMCs) | Indian Oil Corporation | IOC | ₹141.69 |

| Bharat Petroleum Corp. | BPCL | ₹315.55 | |

| Hindustan Petroleum Corp. | HPCL | ₹400.40 | |

| Aviation | InterGlobe Aviation (IndiGo) | INDIGO | ₹5248.50 |

| SpiceJet | SPICEJET | ₹31.70 | |

| Jet Airways (under resolution) | JETAIRWAYS | ₹34.16 | |

| Paints | Asian Paints | ASIANPAINT | ₹2689.00 |

| Berger Paints India | BERGERPAINT | ₹493.70 | |

| Kansai Nerolac Paints | NEROLAC | ₹201.28 | |

| Chemicals | SRF | SRF | ₹2874.70 |

| Aarti Industries | AARTIIND | ₹493.95 | |

| Deepak Nitrite | DEEPAKNTR | ₹1708.00 | |

| Logistics | Delhivery | DELHIVERY | ₹492.15 |

| VRL Logistics | VRLLOG | ₹231.96 | |

| Mahindra Logistics | MAHLOG | ₹387.35 | |

| High Fuel & Energy Cost Companies | UltraTech Cement | ULTRACEMCO | ₹11727.00 |

| Tata Steel | TATASTEEL | ₹185.89 | |

| Ambuja Cements | AMBUJACEM | ₹438.50 |

Why these sectors are vulnerable to high crude prices

- OMCs: Rising crude increases procurement costs and can compress marketing margins if retail fuel prices cannot be raised quickly.

- Aviation: Aviation turbine fuel (ATF) is one of the largest operating expenses, so higher oil prices directly reduce profitability.

- Paints: Petroleum derivatives such as solvents and resins are key raw materials, putting pressure on gross margins.

- Chemicals: Feedstocks like naphtha, benzene, and ethylene become more expensive, raising production costs.

- Logistics: Higher diesel prices increase freight and transportation expenses, squeezing operating margins.

- Cement & Steel: These industries consume large amounts of energy (coal, petcoke, gas, electricity), making them sensitive to sustained increases in global energy prices.

Auto components remain another domestic growth story

Arya is also constructive on India’s auto component industry.

Industry estimates point to 8–10% growth this year, supported by strong domestic demand.

However, exporters remain exposed to risks from possible US tariff changes, making stock selection important within the sector.

Overall, he believes domestic demand-driven businesses remain better positioned than globally exposed sectors.

Long-term outlook remains positive for wealth management companies

Arya continues to favour wealth management companies, asset management firms, depositories and brokerage businesses over the long term.

He described the financialisation of household savings as a multi-decade structural trend that continues to support recurring revenue models.

Retail participation has moderated over the past two years, cooling valuations from their 2023 and 2024 highs.

“These companies are much better placed now, but investors should approach them with a long-term perspective because market volatility will continue through multiple cycles,” he said.

AI correction is a valuation reset, not the end of the growth story

Commenting on the recent weakness in global AI stocks, Arya said the correction reflects a valuation reset rather than a broken investment thesis.

After an exceptional rally in semiconductor stocks, investors are reassessing expectations as major technology companies increasingly develop their own AI chips.

For Indian markets, he believes investors should watch whether foreign institutional flows rotate from Taiwan and Korea back into India.

Rather than one broad AI trade, he expects clear winners and losers to emerge.

Higher crude prices remain the biggest macro risk

Energy prices remain the biggest uncertainty for global markets.

Arya believes India is relatively well diversified in crude imports, with nearly 70% of supplies sourced outside the Strait of Hormuz and imports coming from more than 40 countries.

However, LPG remains a concern since nearly 90% of India’s imported cooking gas passes through Hormuz.

A prolonged disruption could increase inflationary pressures and squeeze corporate margins, even if crude supply remains manageable.

September-quarter earnings may improve only on paper

Arya does not expect a major improvement in September-quarter corporate earnings.

According to him, June-quarter results were heavily impacted by weakness in commodities, particularly oil and gas.

As a result, the September quarter may appear stronger because of an easier comparison base, while underlying earnings momentum remains modest.

“September-quarter earnings may look optically better without the underlying picture improving much,” Arya said.

Higher crude oil prices following the Strait of Hormuz disruption could continue weighing on corporate profit margins.

Here’s what happened today and why traders reacted

Markets reacted to expectations that both the US Federal Reserve and the RBI are likely to keep interest rates unchanged while maintaining a cautious policy stance.

Investors also assessed rising geopolitical risks, elevated crude oil prices and concerns over corporate earnings.

At the same time, Arya’s preference for healthcare, diagnostics and selective domestic sectors reinforced the view that stock picking may outperform broad index investing in the current market environment.

What does this mean for investors?

The outlook suggests investors should prepare for continued market volatility rather than expecting a one-way rally.

Healthcare, hospitals, diagnostic chains and selected auto component companies could offer relatively better earnings visibility, while wealth management businesses remain attractive for long-term investors.

With crude oil prices, inflation and central bank policy likely to dominate market sentiment, disciplined sector selection may prove more rewarding than broad market exposure over the coming quarters.