The 60-Day Hormuz Trap: Why Oil Markets May Be Celebrating Too Early

Key Takeaways

- Brent crude has cooled toward/below the $80 zone after the US-Iran interim agreement and partial Hormuz reopening, but enforcement is still uncertain.

- The 14-point MoU gives negotiators 60 days and promises no-charge Hormuz passage during the interim period, not a permanent toll-free settlement.

- The biggest discrepancies are Israel’s non-participation, the frozen-assets/payment dispute, Hormuz transit conditions, uranium down-blending vs removal, and delayed enforcement.

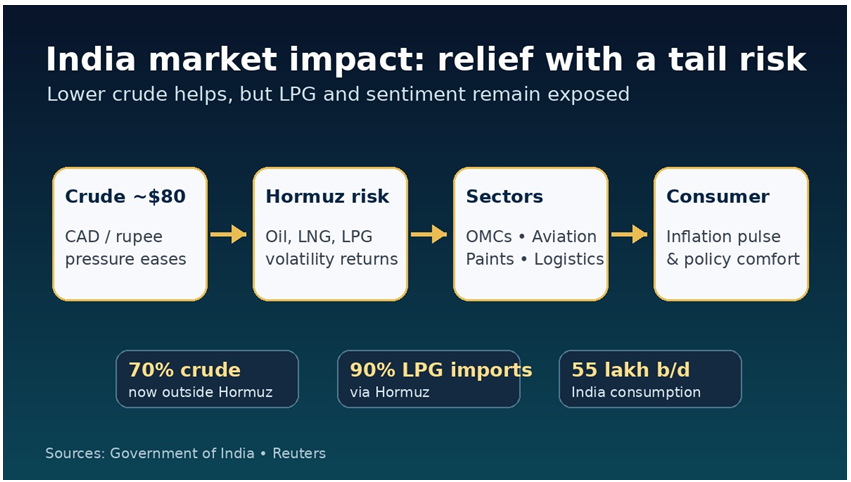

- For India, crude diversification reduces immediate supply risk, but LPG remains exposed because about 90% of LPG imports pass through Hormuz.

Oil traders love a reopening story. Brent has cooled from its April wartime spike toward the $80 zone after the United States and Iran signed an interim agreement and limited tanker movement resumed through the Strait of Hormuz. But the market may be celebrating before the hardest part has even started.

The 14-point memorandum sent by the White House to Congress is not a final peace deal. It is a 60-day bargain to stop the fighting, reopen Hormuz, waive sanctions on Iranian oil exports, discuss frozen assets, and negotiate a final settlement. The fine print is where the risk sits.

Five numbers explain why this story matters for markets: 60 days to turn the MoU into a final deal; at least $300 billion in promised reconstruction and economic-development planning; roughly one-fifth of global oil/liquids supply tied to the Strait of Hormuz; 25 commercial vessel crossings on June 18 versus roughly 120 daily crossings before the war; and for India, about 70% of crude imports now routed outside Hormuz, while about 90% of LPG imports still pass through the same chokepoint.

Graphic: Five numbers behind the Hormuz deal risk.

Read More : Sensex Falls 607 Points, Nifty Drops 155 on Friday as IT Selloff Wipes Weekly Gains

What the 14-point deal actually says

The pact calls for the immediate and permanent end of military operations on all fronts, including Lebanon. It commits the US and Iran to a final deal within 60 days, extendable by mutual consent. The US is to remove the naval blockade within 30 days, issue waivers for Iranian crude and petroleum exports, and work with regional partners on a plan of at least $300 billion for Iran’s reconstruction and economic development.

On Hormuz, Iran promises best efforts for safe commercial passage with no charge for 60 days only, while de-mining and other technical obstacles are addressed within 30 days. On the nuclear side, Iran reiterates that it will not develop nuclear weapons, while the stockpile of enriched material is to be resolved through an agreed mechanism, with the minimum method described as on-site down-blending under IAEA supervision.

That sounds like de-escalation. It is. But it is also a framework that pushes the toughest questions into the next round.

Crack #1: Israel was not in the room

This is the most important political gap. The agreement says military operations should end on all fronts, including Lebanon. But Israel was not part of the US-Iran talks and has said it is not party to the deal. Within hours of a fresh Israel-Hezbollah ceasefire, Reuters reported new Israeli strikes in south Lebanon that killed at least five people.

That means the deal depends on behavior by a player that did not sign it. In game-theory terms, this is not a two-player settlement. It is a three-player game where the US and Iran can agree on paper, but Israel’s actions in Lebanon can still determine whether Iran believes the bargain is being honoured.

Crack #2: The money language is explosive

The MoU says the US will make frozen or restricted Iranian funds and assets fully available for use, with procedures to be agreed during negotiations. It also refers to a plan of at least $300 billion for Iran’s reconstruction and economic development. That is why critics immediately attacked the pact as a financial concession.

Washington is pushing back. Vice President JD Vance said no funds would be released in exchange for signing the agreement and that money would flow only if Iran took verified steps on enriched uranium and inspections. Reuters separately reported claims of UAE-linked transfers to Iran, while the UAE denied that any frozen Iranian funds had been released, transferred or facilitated. The publication-safe line is simple: the pact contains asset and funding mechanisms, but the timing, source, conditions and actual release of money remain disputed.

Crack #3: Hormuz is open, but not normal

The market headline is that tankers have started moving again. The market detail is that Hormuz is still operating under unusual conditions. Reuters reported that at least four tankers entered the strait on Friday and that traffic rose to 25 crossings on June 18, the highest since mid-April but still far below pre-war norms. Iran’s Strait authority also said ships must submit transit requests at least 48 hours before arrival and coordinate routes and timing because of mine-related risks.

Most importantly, the pact says ‘no charge’ for 60 days only. The US says it expects toll-free access in the long term. Iran says future administration and maritime services will be discussed with Oman and other Gulf states. That difference is not a footnote. It is the core of Hormuz leverage.

Crack #4: The nuclear compromise is not a surrender

Iran does not hand over its enriched material under the text as published. The pact refers to resolving the stockpile through a mutually agreed mechanism, with on-site down-blending under IAEA supervision as the minimum methodology. Reuters reported that Trump had wanted the material removed from Iran, which Tehran rejected.

That leaves a political problem for Trump and a verification problem for markets. A deal that lowers oil prices is useful. A deal that leaves room for future nuclear ambiguity is fragile.

Crack #5: Enforcement comes later

The agreement creates an executive mechanism to monitor implementation, but the binding UN Security Council endorsement comes only with the final deal. Until then, the structure is a temporary truce backed by threats, incentives and market relief. Trump has already said the US could resume attacks if Iran violates the deal.

The game theory: everyone wants restraint optics, nobody wants weakness

The strongest way to read the current situation is not as a hidden master plan, but as a signaling game. Trump wants lower oil prices, an exit from direct war, and enough pressure on Iran to claim strength. Public criticism of Israeli strikes helps signal restraint to Iran and to oil-importing allies, while preserving US-Israel strategic alignment if Iran or Hezbollah escalates again.

Graphic: US-Iran-Israel incentives as a three-player game.

Israel has a different incentive. It is not party to the Iran deal, and it sees Hezbollah in Lebanon as an immediate military threat. Its strategic temptation is to degrade Iran-backed networks while Iran is under diplomatic and economic pressure. Too much pressure, however, could give Tehran an excuse to delay talks or tighten Hormuz again.

Iran’s best move is also delicate. It wants sanctions relief, asset access and recognition of its role in Hormuz. But a full closure of the strait or an attack on US assets would give Trump the clean escalation trigger he does not currently have. That is the trap: every player benefits from appearing restrained, but every player also wants to avoid looking defeated.

Why India cannot ignore the fine print

Graphic: India market impact from crude, Hormuz and LPG risk.

For India, lower crude is a direct macro relief. Cheaper oil can support the rupee, reduce inflation pressure, improve the current-account outlook and help energy-consuming sectors such as aviation, paints, logistics and chemicals. But India’s exposure has not disappeared. Government data says India has diversified crude imports, with about 70% now coming via routes outside Hormuz. LPG remains more exposed: India imports about 60% of LPG consumption, and about 90% of those imports pass through Hormuz.

That makes this less of a one-day oil story and more of a 60-day risk story. If Hormuz normalises, crude may stay under pressure and India’s macro trade improves. If Lebanon keeps flaring, or Iran and the US clash over money, uranium or maritime fees, the market may quickly reprice the risk premium.

What traders should watch next

Watch four signals: whether the Switzerland technical talks actually begin and continue; whether Israeli strikes in Lebanon stop for more than a few hours; whether Iran keeps Hormuz transit predictable after the 48-hour request system; and whether Washington can reconcile ‘no money released’ public messaging with the MoU’s asset-release language.

The market is asking whether Hormuz is open. The bigger question is whether the US-Iran-Israel game still rewards escalation.

Track Live : Nifty Trending OI Live

Bottom line

Oil is falling because the market sees a path to peace. But the 14-point pact is not yet peace. It is a 60-day test of whether three players with different incentives can keep the same deal alive. Until Israel’s Lebanon front, Iran’s Hormuz leverage and America’s money-and-nuclear conditions are aligned, the oil market may be pricing calm too early.