India is preparing a dedicated ₹12,000 crore incentive scheme to push local manufacturing of critical battery components, the upstream materials that existing PLI programs have conspicuously left unaddressed.

Key Takeaways

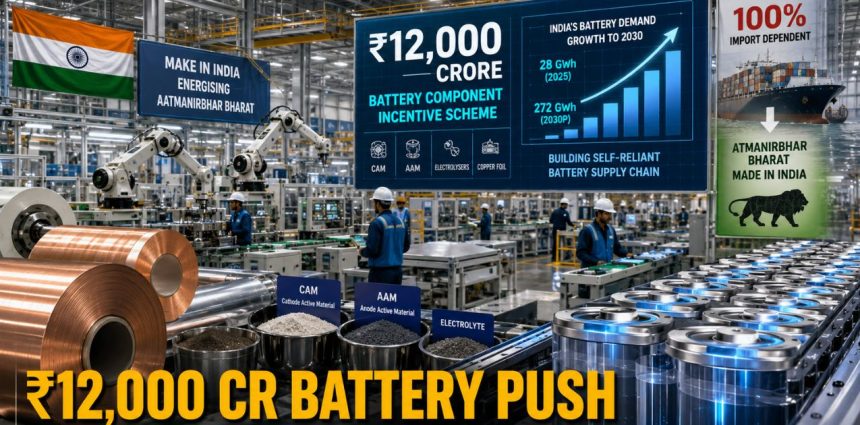

- Government is finalising a ₹12,000 crore scheme specifically targeting CAM, AAM, electrolysers, and copper foil separators

- India is 100% import-dependent for all four component categories today

- The scheme supplements the existing ₹18,100 crore ACC PLI for cell manufacturing, which has delivered just 2.8% of its 50 GWh capacity target

- India will need over 200,000 tonnes of AAM and 400,000 tonnes of CAM by 2030 to support approximately 223 GWh of domestic battery capacity

- Chinese companies hold roughly 80% of global copper foil capacity, followed by Korean manufacturers with around 20%

What Is the ₹12,000 Crore Battery Component Scheme?

India is in the final stages of approving a new financial incentive scheme aimed at building domestic manufacturing capacity for advanced battery cell components.

According to government officials cited by the Economic Times, the scheme will cover four critical upstream materials: cathode active materials (CAM), anode active materials (AAM), electrolysers, and copper foil separators.

“The battery component incentive scheme is in final stages of approval,” a government official told ET, adding that funding will come with attached conditions. “We don’t want companies to import end products or perform last-stage processing and claim incentives,” the official clarified, signalling that the government will actively ringfence value-addition requirements to prevent subsidy arbitrage.

The scheme is distinct from the existing ₹18,100 crore ACC PLI (Advanced Chemistry Cell) programme run by the Ministry of Heavy Industries, which targets cell manufacturing capacity, not the upstream component layer.

Why This Gap Exists — and Why It Matters

Cathode and anode active materials together account for nearly 70% of the total material cost in lithium-ion cells, according to industry representatives.

Despite India having announced approximately 223 GWh of private-sector battery capacity, the country currently imports virtually all of these inputs.

India’s battery demand stood at 28 GWh in 2025 and is projected to scale at a 36.5% CAGR to approximately 272 GWh by FY2030, per IEEFA and JMK Research estimates.

Without a domestic supply chain for the upstream materials, this demand surge will translate directly into surging import bills, and strategic vulnerability.

India is currently 100% import-dependent for lithium, cobalt, and nickel, according to an April 2026 IEEFA analysis.

India imported 18,200 tonnes of lithium compounds worth USD 1.2 billion in 2025, with 68% sourced from China. The new component scheme is designed to structurally reduce this exposure at the processing layer.

India’s Battery Manufacturing Policy Stack: The Full Picture

| Scheme | Outlay | Focus | Status |

|---|---|---|---|

| ACC PLI (Ministry of Heavy Industries) | ₹18,100 Cr | Cell manufacturing (50 GWh target) | Active; 2.8% capacity delivered |

| Battery Component Incentive Scheme | ~₹12,000 Cr | CAM, AAM, electrolysers, copper foil | Final approval stage |

| PLI Auto & EV Components | ₹25,938 Cr | EV vehicles & auto components | Active |

| PM E-DRIVE | — | EV adoption subsidies | Active |

| National Critical Mineral Mission | — | Upstream lithium, cobalt, nickel | Launched Jan 2025 |

Sources: Ministry of Heavy Industries, PIB, Economic Times

The ACC PLI Track Record: Why the Component Scheme Is Urgent

The urgency behind the component scheme becomes clearer when viewed against the ACC PLI’s current delivery record. As of October 2025, only 1.4 GWh, 2.8% of the 50 GWh target, has been commissioned under the scheme, entirely by Ola Electric. No incentives have been disbursed to any beneficiary against the targeted ₹2,900 crore payout.

Investment levels have also lagged significantly, with around ₹28.7 billion committed, approximately 26% of the targeted ₹112.5 billion. The scheme has generated just 1,118 jobs against a target of more than one million.

A key structural reason for this underperformance, identified by IEEFA, is the chicken-and-egg problem: ACC PLI beneficiaries have faced bottlenecks specifically due to the non-availability of upstream components like CAM, AAM, and electrolytes, precisely the materials that the new ₹12,000 crore scheme now targets.

In other words, the cell-manufacturing scheme was always operating without the upstream layer it needed to succeed.

India’s 2030 Demand Requirements: The Numbers

| Component | Estimated Domestic Requirement by 2030 | Current Import Dependence |

|---|---|---|

| Cathode Active Material (CAM) | 400,000+ tonnes | Near 100% |

| Anode Active Material (AAM) | 200,000+ tonnes | Near 100% |

| Copper Foil (battery-grade) | Significant; market est. ₹450–600 Cr in 2026 | 80–85% imported |

| Lithium compounds | Growing; 18,200 tonnes imported in 2025 | 100% |

Sources: Industry estimates via ET; IEEFA; IndexBox India Battery Pack Foils Market 2026

Copper Foil: The Most Concentrated Supply Risk

Of the four components addressed by the scheme, copper foil has the most concentrated global supply chain.

Chinese companies own approximately 80% of global copper foil production capacity for lithium battery applications, with Korean manufacturers accounting for around 20%, according to the International Copper Association of India’s battery supply chain report.

India currently imports 80–85% of its battery-grade copper foil demand, with China accounting for 50–55% of import volume, Japan 20–25%, and South Korea 10–15%.

Domestic production meets less than 20% of current demand, specifically for ultra-thin, high-ductility foils required in advanced cell manufacturing.

On a positive note, Hindalco announced a plan worth ₹45,000 crore in March 2025 to set up India’s first EV copper foil plant, though large-scale domestic supply remains years away from meaningful realisation.

Duty Waivers: The Unresolved Question

A second set of policy decisions linked to the scheme, import duty relief, remains pending. “A call on duty waivers is yet to be taken,” a second government official told ET.

Budget 2026-27 did extend the basic customs duty exemption on capital goods used to manufacture lithium-ion cells for battery energy storage systems, but component-level duty rationalisation has not yet been confirmed.

This matters because the existing tariff structure allows finished battery products to be imported at lower customs duty rates than the raw materials needed to produce them domestically, directly undermining the competitiveness of local manufacturing and creating unutilised Input Tax Credit for domestic producers. Until this inversion is corrected, even a well-funded component scheme may face headwinds.

Stocks and Sectors to Watch

The new scheme, once formally approved, is likely to benefit several domestic players across the battery materials and EV supply chain space. Investors tracking this theme on the NSE and BSE should monitor:

- Battery and specialty chemicals companies with CAM/AAM manufacturing capabilities or announced expansion plans

- Copper producers—Hindalco, Vedanta, Sterlite, given the copper foil push

- EV component manufacturers likely to benefit from a more complete domestic supply chain

- Capital goods and equipment suppliers serving the gigafactory ecosystem

Track real-time FII and DII flows in the EV and capital goods sectors on the [NiftyTrader FII-DII Tool] to identify institutional positioning as policy visibility improves.

Bottom Line

India’s ₹12,000 crore battery component scheme, now in final approval stages, addresses the single most critical gap in the country’s EV supply chain ambitions, the upstream materials layer that the ₹18,100 crore ACC PLI was structurally unable to solve.

With 223 GWh of private-sector battery capacity announced and a 2030 demand requirement running into hundreds of thousands of tonnes of CAM and AAM, the timing of this intervention is not optional.

The real test, as the ACC PLI track record makes clear, will be in execution: realistic domestic value-addition timelines, effective anti-circumvention safeguards, and a resolution of the import duty inversion that currently makes local manufacturing less competitive than simply buying finished components from China.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Please consult a SEBI-registered advisor before making investment decisions.

Data as of June 18, 2026. Source references: Economic Times, IEEFA/JMK Research (January 2026), PIB, International Copper Association of India, IndexBox India Battery Pack Foils Market Report 2026.