OMC Earnings Under Pressure as LPG Losses Hit Rs.500/Cylinder in Q1FY27

India’s oil marketing companies (OMCs) may continue to face earnings pressure despite the recent decline in crude oil prices, according to brokerage firm Prabhudas Lilladher.

The fall in Brent crude below $80 per barrel after the US-Iran ceasefire has improved investor sentiment toward OMC stocks. However, analysts believe the sector’s profitability could remain under stress due to LPG losses, fuel under-recoveries and concerns over a potential rollback of excise duty cuts.

For investors tracking OMC stocks, the key question is no longer whether crude prices are falling—but whether lower oil prices are enough to offset mounting earnings pressures.

Track Live : Stock Market Today

Why OMC Stocks Are Still Facing Earnings Pressure LPG Losses Hit

While crude oil prices have corrected sharply from recent highs, Prabhudas Lilladher expects the first quarter of FY27 to remain challenging for OMC stocks.

The brokerage estimates under-recoveries of around ₹7 per litre and ₹10 per litre during Q1FY27 even after factoring in a ₹10 per litre excise duty cut and capped refining cracks for petrol and diesel.

As a result, lower crude prices may not immediately translate into stronger earnings for oil marketing companies.

“We expect an under-recovery of Rs 7/litre and Rs 10/litre in Q1FY27,” the brokerage said in its report.

Read More : Domestic Flows Push India Cash Market to Rs.1.35L Cr Despite FPI Exit

Core Reasons for Earnings Pressure

- Severe LPG Losses: Liquefied petroleum gas remains the primary drag, with losses estimated at ₹500 per cylinder in Q1FY27 after hitting ₹610–670 in May 2026.

- Fuel Under-Recoveries: OMCs face projected under-recoveries of ₹7 per litre on petrol (Motor Spirit) and ₹10 per litre on diesel (High-Speed Diesel) for Q1FY27.

- Policy & Tax Risks: Profit margins are capped by an assumed ₹10 per litre excise duty cut alongside compressed marketing cracks ($10/bbl for petrol and $15/bbl for diesel).

- Temporary Crude Relief: The post-ceasefire drop below $80/bbl may reverse as global nations aggressively buy oil to replenish depleted strategic reserves.

LPG Losses Remain the Biggest Concern for OMC Stocks

One of the biggest challenges for OMC stocks is the sharp increase in LPG under-recoveries.

According to the brokerage, LPG losses are estimated at nearly ₹500 per cylinder during the quarter.

Management commentary from OMCs during fourth-quarter FY26 earnings calls indicated that LPG under-recoveries widened significantly to around ₹610-670 per cylinder in May 2026 compared with approximately ₹170 per cylinder in April.

The increase has been driven by rising international LPG prices.

Saudi Contract Prices (CP), a key benchmark for LPG imports, are expected to jump 47 per cent quarter-on-quarter during Q1FY27 because of supply disruptions linked to the West Asia conflict.

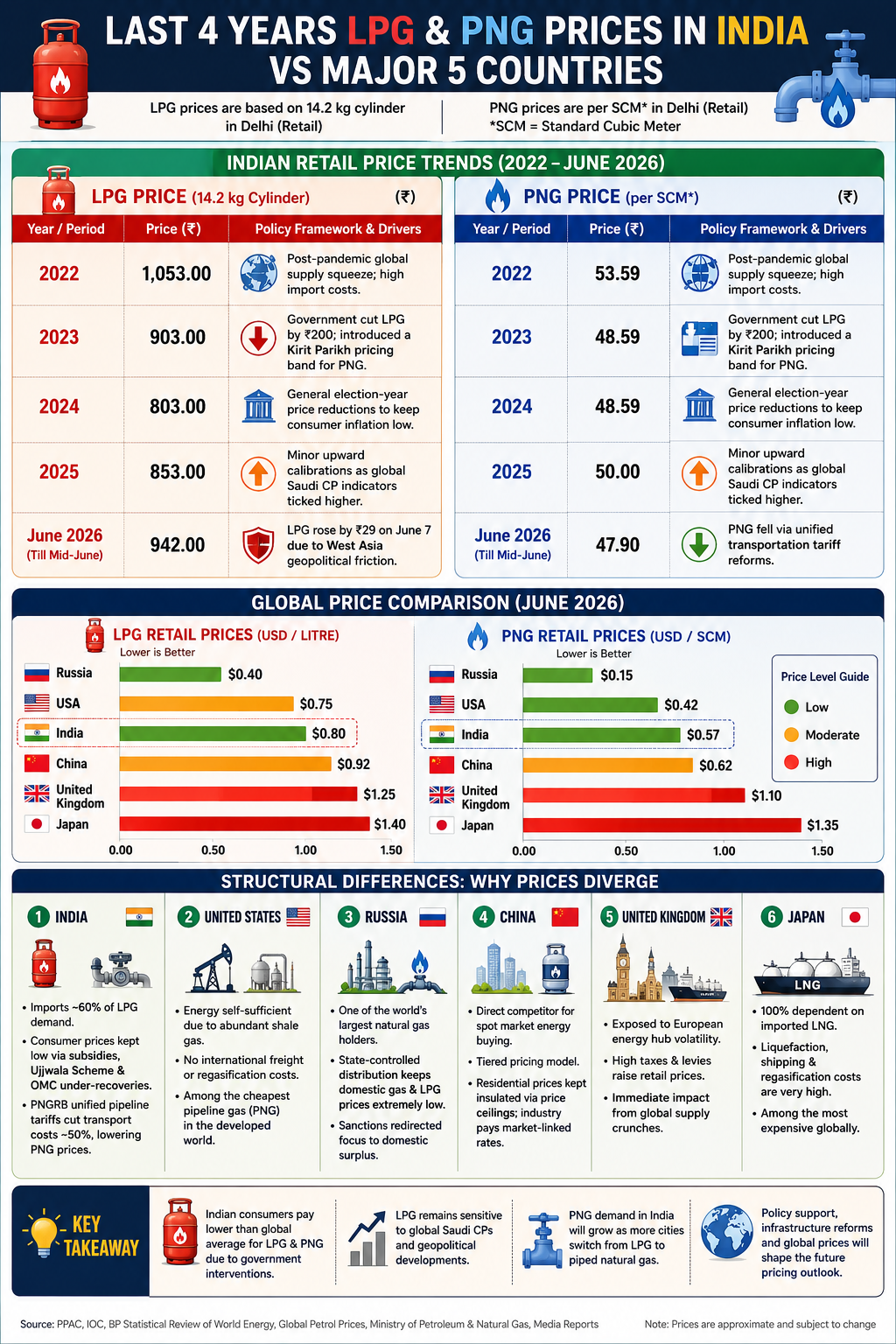

Last 4 Years LPG and PNG Prices in India vs Major Countries

India’s LPG and PNG prices are partially regulated, helping shield consumers from sharp global energy shocks. While international benchmarks such as Saudi Contract Prices influence costs, government subsidies, price caps, and OMC absorption of losses help keep retail prices relatively stable.

| Year | LPG Price (14.2 kg Cylinder, Delhi) | PNG Price (Delhi, per SCM) |

|---|---|---|

| 2022 | ₹1,053 | ₹53.59 |

| 2023 | ₹903 | ₹48.59 |

| 2024 | ₹803 | ₹48.59 |

| 2025 | ₹853 | ₹50.00 |

| June 2026 | ₹942 | ₹47.90 |

Global Comparison (June 2026)

LPG Prices (USD Equivalent)

| Country | LPG Price |

| Russia | $0.40 |

| USA | $0.75 |

| India | $0.80 |

| China | $0.92 |

| UK | $1.25 |

| Japan | $1.40 |

PNG Prices (USD per SCM)

| Country | PNG Price |

| Russia | $0.15 |

| USA | $0.42 |

| India | $0.57 |

| China | $0.62 |

| UK | $1.10 |

| Japan | $1.35 |

Why Prices Differ Across Countries

- India: Uses subsidies, Ujjwala support, and regulated gas pricing to protect consumers.

- USA: Benefits from abundant shale gas production and domestic energy self-sufficiency.

- Russia: Large domestic gas reserves and state-controlled pricing keep costs among the world’s lowest.

- China: Uses a tiered pricing structure, balancing consumer protection with market-linked rates.

- UK & Japan: Highly exposed to global energy markets, import costs, and taxes, resulting in higher retail prices.

Last 4 Years Crude Oil Price Comparison: India vs Global Benchmarks

The Indian Crude Basket, which reflects the weighted average cost of crude imported by India, closely tracks Brent crude but can trade at a premium or discount depending on freight costs, supply disruptions, and India’s import mix. Russia’s discounted oil exports have played a major role in reducing India’s effective import costs since 2022.

| Year | Brent Crude Avg ($/bbl) | WTI Crude Avg ($/bbl) | Indian Crude Basket Avg ($/bbl) |

|---|---|---|---|

| 2022 | 100.9 | 94.3 | 93.1 |

| 2023 | 82.5 | 77.7 | 82.6 |

| 2024 | 80.5 | 76.6 | 79.0 |

| 2025 | 69.1 | 65.2 | 64.0 |

| June 2026* | 80–85 | 76–80 | 78–85 |

*Approximate June 2026 levels after the sharp correction following the easing of US-Iran tensions. Brent had surged above $110 during the conflict before retreating.

How the Top 5 Oil Powers Influence India’s Crude Costs

Russia – India’s Largest Supplier

- Russia remains India’s biggest crude supplier.

- Discounted Russian Urals crude helped India reduce import costs during periods when Brent exceeded $100 per barrel.

- Russian supplies became a key cushion during the 2022 energy crisis and the 2026 Middle East conflict.

Saudi Arabia – OPEC’s Key Producer

- Saudi Arabia remains one of India’s most important traditional suppliers.

- OPEC+ production cuts significantly influenced global oil prices during 2023-2025.

- Higher Saudi Contract Prices directly affect India’s LPG and crude import bill.

United States – Shale Production Leader

- Record US shale output helped cap global oil prices in 2024 and 2025.

- WTI pricing serves as a global benchmark influencing Brent and broader energy markets.

Canada – Growing Non-OPEC Supply

- Expansion of export infrastructure increased global crude availability.

- Additional non-OPEC barrels helped offset supply restrictions from OPEC+ producers.

China – India’s Largest Demand Competitor

- China and India are among the world’s largest crude importers.

- Chinese demand recovery or strategic reserve purchases often push global crude prices higher, impacting India’s import costs.

Excise Duty Rollback Could Create Another Headwind

Apart from LPG losses, Prabhudas Lilladher highlighted the possibility of a phased rollback of fuel excise duty cuts as another major risk for OMC stocks.

The brokerage believes the government’s ₹10 per litre excise duty reduction was introduced as a temporary measure during a period of elevated crude prices.

With oil prices now moderating and retail fuel prices adjusted higher, the government could gradually withdraw the benefit.

“The overhang of a rollback in excise duty cuts of Rs 10/litre remains a key pressure point for OMCs,” the brokerage noted.

The report estimates that the Centre continues to face an annual revenue impact of nearly ₹1.7 lakh crore due to the excise duty reduction.

What Investors Should Watch Next

LPG Under-Recoveries

- LPG remains the biggest earnings drag for OMCs.

- Under-recoveries surged from about ₹170/cylinder in April 2026 to ₹610–670/cylinder in May 2026.

- Any government compensation could significantly improve earnings visibility.

Excise Duty Rollback

- The ₹10/litre excise-duty cut remains a key overhang.

- A phased rollback could reduce OMC marketing margins and pressure profitability.

Crude Oil Volatility

- Brent has cooled, but the decline may not last.

- Countries rebuilding strategic petroleum reserves could support crude prices and limit further downside.

OMC Investor Dashboard for FY27

| Trigger | Positive Scenario | Negative Scenario |

|---|---|---|

| LPG Losses | Government compensation announced | Under-recoveries remain elevated |

| Excise Duty | No rollback or delayed rollback | Phased excise restoration reduces margins |

| Crude Oil | Brent remains below $75-$80 | Crude rebounds due to reserve rebuilding |

| Refining Margins | Strong cracks support earnings | Weak refining spreads hurt profitability |

| Fuel Demand | Robust consumption growth | Higher retail prices impact demand |

Why Crude Prices May Not Stay Low for Long

Prabhudas Lilladher expects crude oil prices to soften further if geopolitical tensions continue to ease and shipping activity through the Strait of Hormuz normalises.

However, the brokerage warned that the decline may be temporary.

Countries that depleted strategic petroleum reserves during the conflict are expected to rebuild inventories, creating fresh demand for crude oil.

At the same time, Iranian oil exports could resume more quickly following the easing of tensions.

The combination of reserve replenishment and recovering demand could support crude prices and prevent a prolonged decline.

For OMC stocks, that means the benefits of lower crude oil prices may be limited, while earnings pressures from LPG losses and under-recoveries continue to dominate the near-term outlook.