Is Citizenship by Investment Worth It for Indian Traders ?

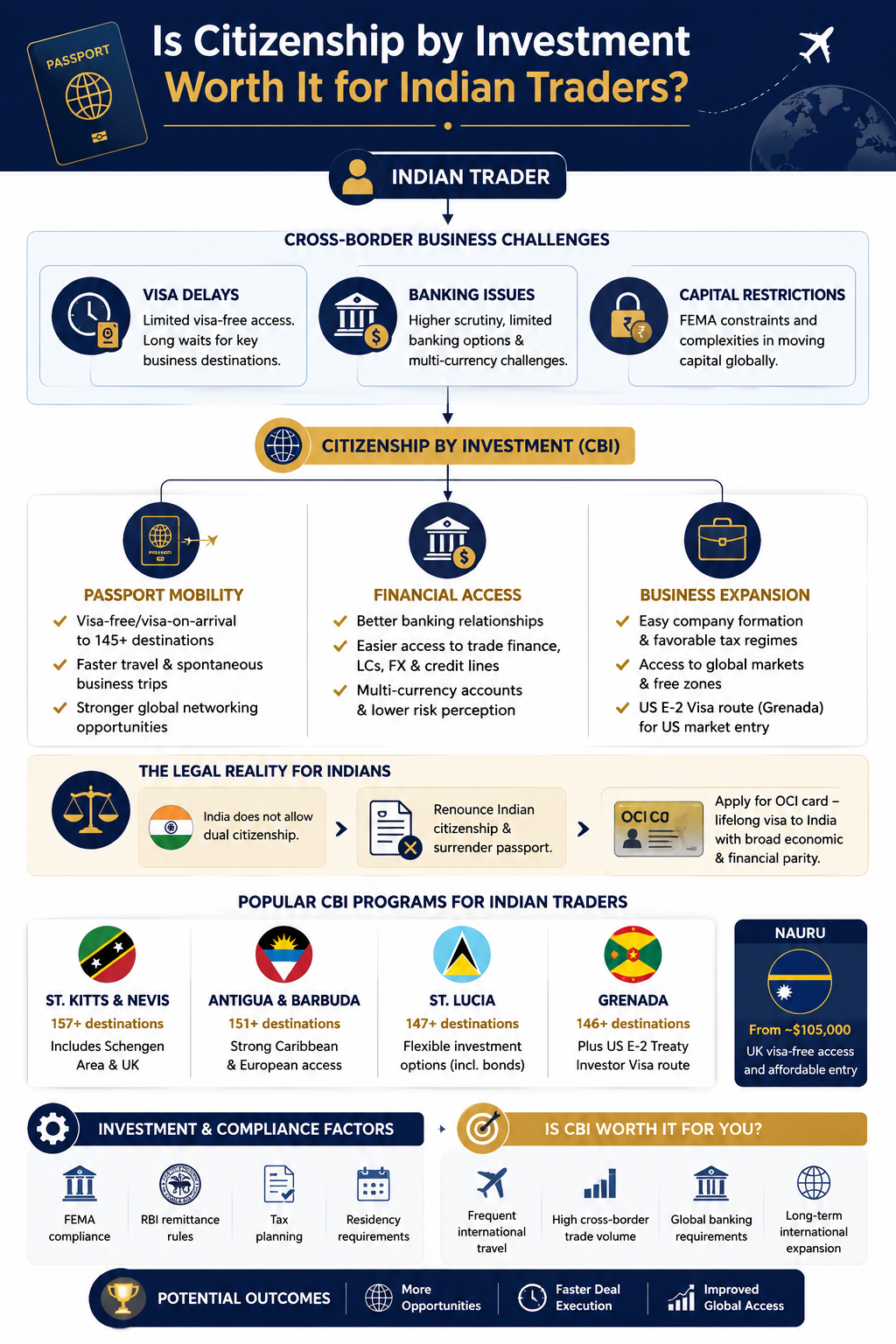

You’re an Indian trader with serious cross-border ambitions. And somewhere along the way, you’ve hit the same walls that almost every Indian business owner hits when trying to operate globally — a passport that requires visa queues for nearly every major market, banking relationships that are harder to open than they should be, and capital controls that slow everything down.

Citizenship by investment (CBI) is increasingly how successful Indian traders are solving this problem. But it’s not a simple decision, and it’s definitely not for everyone.

Here’s what you actually need to know before making a move.

Track Live : Live Stock Screener for Indian Markets

Why Indian Traders Face a Unique Set of Problems

The Indian passport currently provides visa-free or visa-on-arrival access to around 58 destinations — a number that looks quite modest when you consider that most of the world’s major trading hubs sit firmly in the “requires prior visa” column.

Schengen Europe, the UK, the United States — these are not fringe markets. They’re the places where import-export traders source goods, where commodity traders interact with counterparties, and where fintech entrepreneurs close deals. Waiting three to six weeks for a UK business visa when a supplier meeting comes up at short notice isn’t just inconvenient. It costs deals.

Layer on top of that the Foreign Exchange Management Act (FEMA) constraints around moving capital abroad, the “country risk” perception some international banks apply to Indian residents, and the challenge of opening multi-currency accounts as an India-domiciled individual — and the friction compounds quickly.

CBI programs, particularly in the Caribbean and Oceania, address several of these friction points simultaneously. The question is whether that value justifies the investment and the irreversible step of giving up Indian citizenship.

Also Read : Nifty at 24,168, Sensex Gains 254 Points on Crude Dip, Rupee Rises for 5th Session

The Passport Power Gap Is Bigger Than Most Traders Realize

The numbers here are stark. Consider what the leading CBI programs actually deliver in terms of mobility:

- St. Kitts & Nevis — 157+ visa-free/visa-on-arrival destinations, including the EU Schengen Area and UK

- Antigua & Barbuda — 151+ destinations, with strong Caribbean and European access

- St. Lucia — 147+ destinations, flexible investment options including government bonds

- Grenada — 146+ destinations, plus the uniquely valuable US E-2 Treaty Investor Visa route

Even Nauru, one of the newest and most affordable programs at around $105,000 entry, specifically highlights UK visa-free access — which alone is meaningful for traders operating between Asia and Europe.

For most Indian traders, the practical translation of these numbers is this: fewer cancelled trips, faster decisions, and the ability to walk into a trade fair in Frankfurt or Birmingham on two weeks’ notice rather than two months’.

What CBI Actually Does for Your Trading Business

Banking and financial access

One of the less-discussed but more tangible benefits of CBI is what it does for your banking relationships. Holding a Caribbean or Oceanian passport, particularly while residing in that jurisdiction for tax purposes, significantly reduces the “emerging market risk” flags that international banks apply when reviewing new account applications.

Trade finance instruments — letters of credit, FX hedging lines, merchant accounts — are all easier to access when your jurisdictional profile is cleaner. For traders moving millions of dollars in goods annually, even a marginal improvement in financing terms compounds into real money.

Company formation and market entry

Several CBI jurisdictions pair straightforward corporate frameworks with favorable tax treatment on international business income. This is particularly relevant for commodity brokers routing transactions through offshore entities, import-export operators using free zones, and crypto or fintech traders who need access to regulated exchanges that restrict Indian residents.

Grenada’s E-2 route deserves specific attention here. A Grenadian citizen can apply for the US E-2 Treaty Investor Visa, which allows them to establish and operate a US business entity. For traders with US market ambitions — think Chicago commodity exchanges or New York-based importers — this creates an entry pathway that simply doesn’t exist for Indian passport holders.

A practical scenario: the electronics importer

Consider a Mumbai-based electronics importer sourcing components from Germany and the Netherlands. Prior to CBI, every supplier visit required a Schengen visa application with supporting documentation, financial statements, and a wait that made last-minute procurement trips impossible.

After acquiring St. Kitts & Nevis citizenship, that same trader travels to EU suppliers twice a year without pre-application. Direct factory relationships replace distributor relationships. Landed costs drop because the trader can negotiate on-site rather than remotely. The passport paid for itself within three to four years in margin improvement alone — before accounting for any banking or tax benefits.

The Legal Reality: India Doesn’t Allow Dual Citizenship

This is the part that stops many Indian traders in their tracks, and it should be approached with complete clarity rather than glossed over.

India does not permit dual citizenship under any framework. An Indian citizen who voluntarily acquires foreign citizenship through CBI must renounce their Indian citizenship and surrender their Indian passport. This is a legal requirement, not a technicality that can be worked around.

What comes after is the Overseas Citizen of India (OCI) card — a lifelong multiple-entry visa to India that provides broad parity with Non-Resident Indians in economic, financial, and educational matters. OCI is not dual citizenship, as the Ministry of External Affairs is explicit about this, but it does allow you to maintain meaningful personal and business ties to India without holding Indian citizenship.

So the actual decision sequence for an Indian trader pursuing CBI looks like this:

- Acquire foreign citizenship through a CBI program

- Formally renounce Indian citizenship

- Apply for OCI status to maintain India access

For traders whose businesses are India-anchored but globally active, this is often workable. For those whose identity, property rights, or future plans are deeply tied to Indian citizenship specifically, it’s a harder trade-off.

FEMA, Remittance Rules, and Tax Implications

Moving capital abroad for a CBI investment must comply with FEMA and RBI regulations. The Liberalized Remittance Scheme (LRS) allows Indian residents to remit up to USD 250,000 per financial year — which means investments in the $200,000–$325,000 range typical of Caribbean programs may require staging across multiple years or the use of corporate structures.

The tax picture also shifts when residency moves. India taxes residents on global income but limits taxation of non-residents to Indian-source income only. A trader who genuinely relocates tax residency to a Caribbean jurisdiction with territorial or zero-tax treatment on foreign-source income may access significant tax optimization — but only when residency is substantive, not cosmetic. Transfer pricing rules, permanent establishment risk, and disclosure obligations all apply and require proper professional structuring.

This is not a “set and forget” transaction. It requires ongoing compliance across multiple frameworks simultaneously.

Choosing the Right Program: A Trader’s Matrix

For most Indian traders evaluating CBI seriously, the decision narrows to a handful of programs based on three variables: cost, processing speed, and the specific mobility or business benefit they need.

St. Kitts & Nevis is the strongest all-around Caribbean passport, processing in around three to four months from a $250,000 donation. It’s the default choice for traders who want maximum passport power and fast turnaround.

Grenada is the strategic pick for traders with US market ambitions, given the E-2 treaty benefit. Donations start at $235,000 with processing around seven to eight months.

Vanuatu processes in two to three months from $130,000 — the fastest program available. For traders who need a second passport quickly and primarily want to resolve documentation friction rather than maximize mobility, it’s a practical entry point.

Malta’s citizenship by merit framework sits at the premium end — processing over twelve to twenty-four months and requiring an exceptional contribution. For traders seeking full EU citizenship with access to 180+ destinations and European business establishment rights, it remains the highest-value program in the market.

Read More : EPF Interest Rate 2025-26 Approved at 8.25%, EPFO to Credit 7 Crore Members This Month

Working With the Right Advisors

Given the complexity of the India-specific legal framework, the FEMA staging requirements, and the irreversibility of renouncing citizenship, working with an experienced investment migration firm isn’t optional — it’s essential.

Global Residence Index is one of the most established advisory firms in this space, with over nine years in the industry and more than 1,000 clients served across their five global offices. Their approach is notable for the emphasis on pre-due-diligence screening before any application is submitted — which is particularly valuable for Indian traders with complex business structures or multi-jurisdictional income who might otherwise face avoidable complications during government review.

For Indian traders specifically, working with advisors who understand the intersection of FEMA compliance, OCI transition, and CBI investment structuring makes a material difference in both timeline and outcome. You can explore their full program offering through Global Residence Index’s CBI overview to understand which programs currently align with your profile.

When CBI Is Actually Worth It for Indian Traders

CBI makes strong sense for Indian traders who have substantial cross-border activity, who can genuinely use stronger passport access for business travel, and who are ready to manage the OCI transition carefully. For an active import-export trader with $5–10 million in annual volume, even a 2–3% improvement in terms negotiated through better direct supplier access can return the program cost within three to five years.

It makes less sense for traders whose operations are primarily domestic, for those who are not prepared to renounce Indian citizenship, or for anyone approaching it primarily as a tax minimization strategy without genuine residential relocation.

The question isn’t really “is CBI worth it?” The better question is: what is the specific cost, in lost deals, banking friction, and visa delays, of not having a stronger passport? For many Indian traders operating at scale internationally, that cost is already material — they just haven’t calculated it yet.