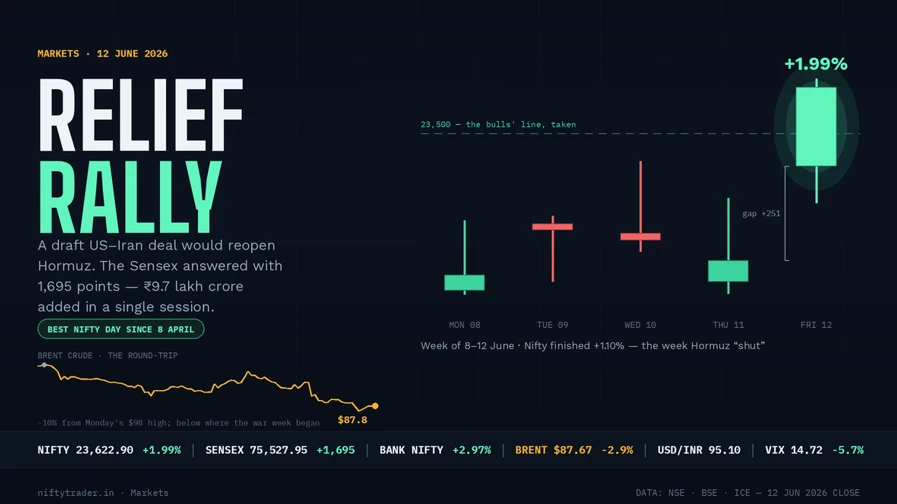

Mumbai | June 12, 2026 — Twenty-four hours after Iran declared the Strait of Hormuz closed, Dalal Street staged its biggest party in two months. A draft US–Iran agreement that would reopen the strait and ease oil sanctions, confirmed by Iranian state media, talked up by President Trump, and still unsigned, sent the Sensex up 1,695 points (+2.30%) to 75,527.95 and the Nifty 50 up 461 points (+1.99%) to 23,622.90, adding roughly ₹9.7 lakh crore to investor wealth in a single session, per BSE market-cap data.

Brent crude, which spiked toward $96 on Thursday’s closure declaration, collapsed to $87.67, below where it traded before Iran shut the strait. India VIX sank 5.7% to 14.72. And in one of the cleanest rotations you will ever see on a single tape, the trades that fed on this war for four months, upstream oil, defence, tanker premiums, were sold to fund the trades the war had crushed.

Here is what was actually agreed upon (and what wasn’t), why banks and oil-marketing companies led the charge, and what history says about ceasefire rallies and the levels that now decide whether 24,000 is next.

What was actually agreed to and what wasn’t

Strip the euphoria, and the facts are narrower than the tape suggests. According to Iranian state media reports carried by international wires on Friday, the draft framework under negotiation would reopen the Strait of Hormuz to commercial shipping, ease oil-related sanctions on Tehran, and release a tranche of frozen Iranian assets. President Trump told reporters a deal was close, and several outlets ran with “the war is over.”

Tehran’s own messaging was pricklier. Iranian officials stressed the strait would reopen under Iranian “maritime coordination rules,” not US control, and, as if to underline the point, Iranian forces stopped a tanker in the strait on Friday morning for allegedly violating those rules.

Mr. Trump, for his part, acknowledged US forces had been “taking out many ships” in the waterway this week. The human cost is real and continuing: reports on Friday confirmed Indian crew members were among the casualties of this week’s tanker strikes, a reminder that for the seafarers who move India’s oil, this is not yet peace.

So Friday’s rally is a bet on a signature that does not yet exist. That is not a reason to dismiss it; markets correctly front-ran the June 2025 ceasefire too, but it defines the risk: every leg of Friday’s move reverses if the draft dies.

The scoreboard: a ₹9.7 lakh crore Friday

The numbers deserve a beat of appreciation. The Nifty gapped up 251 points at the open, it never looked back, never filled the gap, and closed near the day’s high of 23,645. The 1.99% gain ranks as the index’s third-best session of the past twelve months, behind only April 8’s short-covering melt-up (+3.78%) and February 3’s budget-week surge (+2.55%).

Bank Nifty did even better, +2.97% to 56,814.80, smashing through the 55,600 ceiling that had capped it all week. Breadth was emphatic; the Nifty Midcap 100 rose 2.43%, outpacing large caps.

Two quieter numbers matter more. First, India VIX at 14.72: the fear gauge has now fully round-tripped the entire Hormuz episode and sits below where it was before Monday’s ₹5-lakh-crore crash.

Second, the weekly close: from last Friday’s 23,367 to this Friday’s 23,623, the Nifty finished +1.10% in the week Iran declared the world’s most important oil chokepoint shut. Let that sentence sink in, it is the single best summary of how much war premium this market had already paid in March and April.

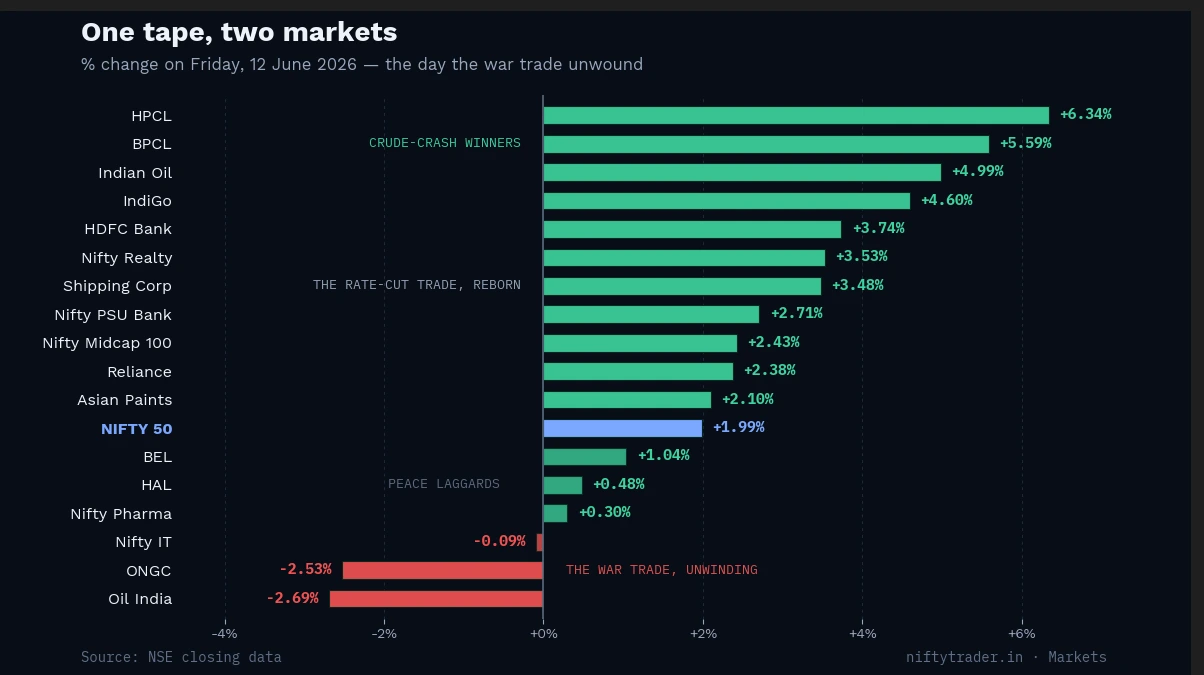

One tape, two markets: the war trade unwound

Friday’s real story isn’t the index; it’s the violence of the rotation underneath it.

The crude-crash winners. Oil-marketing companies, bleeding on frozen pump prices since crude crossed ₹10,000 a barrel in rupee terms, exploded: HPCL +6.3% to ₹388.90, BPCL +5.6% to ₹302.35, and Indian Oil +5% to ₹140.94, IOC’s best day in months, lifting it off the 52-week-low zone it was scraping on Thursday.

Every $1 off Brent flows almost directly into their marketing margins while retail prices stay administered. IndiGo (+4.6% to ₹4,709.70) told the same story through jet fuel and Asian Paints (+2.1%) through crude-derivative inputs.

The rate-cut trade, reborn. HDFC Bank: +3.7%; Nifty PSU Bank: +2.7%; Nifty Realty: +3.5%, the leadership board reads like an RBI-easing playbook, and that is exactly what it is (more below).

The peace laggards. Defence, the most crowded “war winner” of 2026, barely participated: HAL +0.5%, BEL +1% against a +2% index; the relative underperformance of 100–150 basis points on the day peace broke out is the market quietly de-rating the order-flow-forever narrative.

Nifty Pharma (+0.3%) and FMCG (+0.6%) lagged as defensives do in a risk-on tape. And Nifty IT actually closed red (−0.09%); a +2% market could not drag the sector green, confirming what we wrote on Thursday: the old “weak-rupee hedge” reflex is broken, and a strengthening rupee (95.10, up from 95.76) now works against it.

The war trade, unwinding. ONGC is at −2.5% to ₹246.20 and Oil India is at −2.7% to ₹417.80, already wounded by June’s windfall-levy revision, upstream now faces $87 crude too: taxed on the way up, repriced on the way down.

GE Shipping went out flat as war-risk freight premiums, the tanker bull case, started deflating, even as Shipping Corp. (+3.5%) caught a broader PSU bid. Nifty Energy rose just 1.5%, dragged by upstream even with Reliance up 2.4%, and still sits about 5–6% below its 52-week high, the “obvious” war hedge underperformed a peace rally and never paid during the war’s peak either.

The quiet driver: the rate-cut trade is back

Peace headlines explain the gap-up. The composition of the rally, banks, PSU lenders, realty, and midcaps is about something more durable: the inflation math just swung hard in the RBI’s favour.

Multiply Friday’s Brent ($87.67) by Friday’s rupee (95.10), and India’s true oil price is roughly ₹8,340 a barrel, down 5% in a day, down 26% from the April 29 record of ₹11,203, and within sight of the ₹7,500 “all-clear” line we flagged on Thursday.

Run the standard rule of thumb in reverse: every sustained $10/barrel decline narrows the current account deficit by 0.3–0.4% of GDP and takes 30–35 basis points off CPI. On June 5 the RBI held the repo rate at 5.25% and cut its growth forecast to 6.6% with one stated swing factor: crude. A week later, that swing factor is collapsing.

That is why in the most rate-sensitive corners of the market, HDFC Bank’s +3.7% was its best day of the quarter; realty’s +3.5% led every sector, outran even the oil-relief names in aggregate.

If Brent holds in the $80s, an August rate cut moves from “hope” to “base case,” and Friday was the market starting to price it.

Watch Monday’s FII/DII numbers; Friday’s provisional flows will show whether foreign money, a net seller through the war months, is chasing this turn.

What ceasefire rallies do next: the record

We ran this study on Thursday for oil shocks; here is the sequel for de-escalation days specifically.

| Episode | The relief day | What happened next |

|---|---|---|

| Jan 2020 — Soleimani de-escalation | Sensex +1.2% as Iran’s response proved symbolic | Rally held; market made new highs within weeks (until Covid) |

| Mar 2022 — Russia peace-talk hopes | Nifty bottomed Mar 8, +15% in four weeks | Durable, supply was rerouted, not lost; lows never retested |

| Jun 2025 — Israel–Iran ceasefire | Nifty jumped the morning after the Jun 24 truce | Never looked back; the run ended at 26,373 in Jan 2026 |

| Apr 8, 2026 — mid-war short-covering | Nifty is +3.78%, with no resolution attached | Stalled at 24,231 within a week, then faded, the warning row |

| Jun 12, 2026 — US–Iran draft deal | Nifty +1.99%, ₹9.7 lakh crore added | Open |

The pattern: relief rallies attached to a real supply normalization hold; relief rallies attached to hope alone stall. April 8 is this rally’s cautionary twin, a bigger one-day gain than Friday’s, built on nothing but positioning, that died at 24,231. The difference this time is a documented draft with terms. The risk is that the draft is the hope.

The verification, once again, is not on a stock screen: daily tanker transits through Hormuz, Lloyd’s war-risk premiums, and whether Brent stays below $90. If ships move and insurance reprices down, this rally has fuel. If Tehran’s “coordination rules” become Friday’s tanker seizure repeated, it doesn’t.

The new map: levels that decide 24,000

- Nifty 50: The breakout level of 23,500 is now the floor that matters, Thursday’s ceiling, and Friday’s springboard. Below it sit 23,400 and Friday’s low of 23,314; the big vulnerability is the open gap at 23,162–23,413, which a deal collapse would target fast. Above, Friday’s high was 23,645, then the 23,860–24,090 band from our Thursday playbook, then 24,231, April’s recovery high and the gateway to 24,500+.

- Bank Nifty: blasted through 55,600, which flips to support (Friday’s low 55,727 confirms). Friday’s high, 56,867, is the immediate hurdle, then the 57,456 April swing high. The 52-week high near 61,765 remains a different conversation.

- India VIX 14.72: Option premiums are the cheapest since the war began, read it either as the all-clear or as cheap insurance, depending on your book. Live positioning on the option chain will show whether Monday’s writers crowd the 23,500 put.

- Brent in rupees: ₹8,340 and falling. Under ₹7,500 is the full all-clear; back above ₹9,000–10,000 means the deal is wobbling.

What should investors actually do?

The principles from Thursday aged well in twenty-four hours; here is the Friday-evening update.

- Don’t chase a +2% gap day with leverage. The easy 461 points are gone. History’s relief rallies rewarded holding, not buying, the second morning with borrowed conviction, especially with an unsigned draft underneath.

- If you sold the panic, the market just billed you. Monday’s sellers near 23,070 paid a 2.4% tax by Friday. The compounding lesson of 2019, 2022, 2025, and now: exits made on war headlines are almost always repurchased at higher prices. Equity SIP inflows held through May; those rupees are the quiet winners again.

- Respect the gap. An open gap at 23,162–23,413 is this rally’s receipt. Position sizes should assume a deal-collapse headline can fill it in one session.

- Rotate with the regime, not the rear view. The market just told you its post-war pecking order: rate-sensitive and oil-consuming over upstream, defence and the IT “hedge.” Fighting Friday’s tape to average down the war trade is a thesis, not a hedge.

- Pre-write the failure case. Brent back over $92, VIX through 18, or Tehran walking out—decide now what each does to your book. The investors who navigated April best were the ones who had written down their invalidation levels in March.

This is general market education, not personalised investment advice; position sizes and risk tolerance differ, so consult a SEBI-registered investment adviser before acting.

The Bottom line

On Thursday the market refused to panic about a closed strait; on Friday it refused to wait for a signed peace. Both reactions came from the same place: four months and a 16% drawdown of war already in the price.

A ₹9.7-lakh-crore day built on a draft is both genuinely rational and genuinely fragile, rational because crude at ₹8,340 rewrites India’s inflation math and fragile because Iran stopped a tanker the same morning the world declared the war over. Hold 23,500, and the rally has earned the right to test 24,000. Watch the ships, not the statements; that rule made money in both directions this week.

FAQs

Why did the stock market rise so sharply today?

A draft US–Iran deal, reported by Iranian state media and confirmed in intent by President Trump, would reopen the Strait of Hormuz and ease oil sanctions. Brent crude fell to $87.67, below pre-crisis levels, slashing India’s import costs and inflation risks. The Sensex rose 1,695 points, and BSE-listed market value grew about ₹9.7 lakh crore.

Is the US–Iran war actually over?

No agreement has been signed. Iran insists it will not cede control of Hormuz, stopped a tanker on Friday under its “maritime coordination rules,” and strikes occurred as recently as this week. The market is pricing a high probability of a deal, not a completed one.

Why did ONGC and Oil India fall on a big rally day?

Upstream producers are the “war trade”: they benefit from high crude. With Brent down 10% from Monday’s high and the June 1 windfall levy still capping realisations, both fell about 2.5–2.7% even as the index jumped 2%.

Are OMC stocks like HPCL, BPCL and IOC a buy after this rally?

Their earnings math improves directly with every dollar off Brent while pump prices stay frozen — that is why they rose 5–6% on Friday. But the move is event-driven and reverses if the deal fails; valuation, your horizon and risk appetite should decide, ideally with a SEBI-registered adviser.

Will the Nifty cross 24,000 now?

The path runs through 23,860–24,090 and then April’s high of 24,231. It stays open while the Nifty holds 23,500 and Brent holds below roughly $90. A breakdown of the draft deal targets Friday’s open gap at 23,162–23,413 first.

Will petrol and diesel prices come down in India?

Crude in rupee terms is back to about ₹8,340 a barrel, far below April’s ₹11,203 record. The first effect is margin repair for oil-marketing companies after months of losses; meaningful retail price cuts would likely need crude sustained nearer ₹7,500/bbl and a political green light.