Suryoday Small Finance Bank tops the senior citizen FD chart at 8.10% for five years, well ahead of public sector banks topping out near 7.45% and foreign banks near 7.10%. Here’s the full comparison, plus DICGC cover, TDS, and Form 15H rules for FY 2026-27.

Key Takeaways

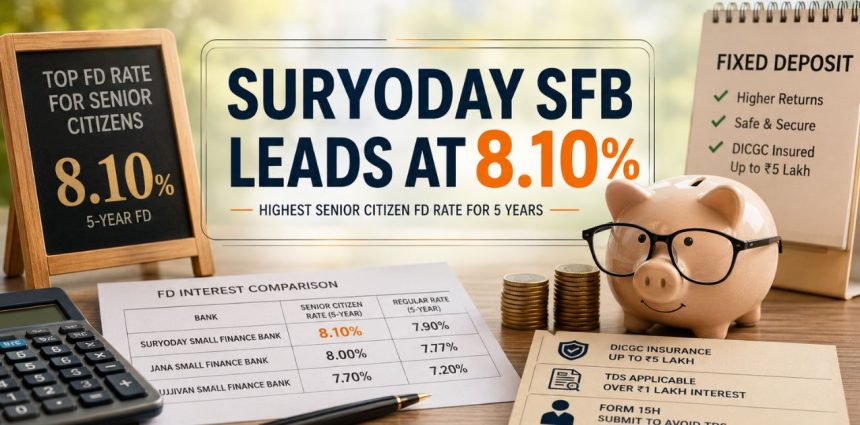

- Small finance banks lead the chart: Suryoday SFB offers 8.10% to senior citizens on a 5-year FD, followed by Jana SFB (8.00%) and Ujjivan SFB (7.70%).

- Among public sector banks, Bank of India offers the highest senior citizen rate at 7.45%, with Indian Bank, Bank of Baroda and Central Bank of India trailing.

- Foreign banks operating in India, Standard Chartered, Deutsche Bank, HSBC, offer comparatively modest rates, topping out around 7.10%.

- DICGC insurance covers only ₹5 lakh per depositor per bank, regardless of which category of bank you choose.

- TDS applies once a senior citizen’s interest from one bank crosses ₹1 lakh a year; Form 15H can stop it if final tax liability is nil.

Also Read: Fixed Deposit: Plant the Seeds of Your Future

Small Finance Banks Still Lead On Rate

Suryoday Small Finance Bank’s five-year senior citizen rate stands at 8.10%, revised in March 2026. Jana SFB follows at 8.00% (per its June 2, 2026 rate notice) and Ujjivan SFB at 7.70%.

| Bank | Senior Citizen Rate | Regular Rate | Effective From |

|---|---|---|---|

| Suryoday Small Finance Bank | 8.10% | 7.90% | March 6, 2026 |

| Jana Small Finance Bank | 8.00% | 7.77% | June 2, 2026 |

| Ujjivan Small Finance Bank | 7.70% | 7.20% | Current card rate |

Data as of June 20, 2026, for deposits below ₹3 crore. Rates are subject to change — confirm with the bank before booking.

Public Sector Banks: Senior Citizen Rates (1–10 Year Tenures)

Public sector banks trail small finance banks by 60–90 basis points on their best senior citizen rates but offer the comfort of larger balance sheets and wider branch networks.

| Bank | Senior Citizen Rate (up to) |

|---|---|

| Bank of India | 7.45% |

| Punjab & Sind Bank | 7.20%–7.35% |

| Indian Bank | 7.30% |

| Bank of Baroda | 7.00%–7.25% |

| Central Bank of India | 7.20% |

Check Live: Indian Bank FD Calculator

Foreign Banks: A Smaller Slice Of The Pie

Foreign banks operating in India serve a smaller retail FD base, and their senior citizen rates generally sit below both SFBs and PSU banks on comparable tenures.

| Bank | Rate (1–5 Year Tenures) |

|---|---|

| Standard Chartered Bank | Up to 7.10% |

| Deutsche Bank | Up to 7.00% |

| HSBC Bank | Up to 6.00% |

Why The DICGC Insurance Limit Matters

Whichever category of bank you choose, DICGC insurance covers only ₹5 lakh per depositor per bank, savings, current, and FD balances combined. Splitting a large deposit across two or three banks, rather than chasing the single highest rate, keeps the full amount protected.

Spreading Deposits: What Experts Suggest

Financial advisors typically recommend a three-part approach for senior citizens comparing these options: stay within the ₹5 lakh DICGC cover per bank by spreading deposits across institutions, use small finance banks selectively for the rate premium rather than parking everything there, and match the tenure to when you’ll actually need the money rather than chasing the longest lock-in for a marginally higher rate.

When Does TDS Apply to Your FD Interest?

Banks deduct 10% TDS once a senior citizen’s annual FD interest from a single bank crosses ₹1 lakh. This threshold applies per bank, so interest spread across three banks won’t trigger TDS until each individual bank crosses ₹1 lakh.

TDS isn’t a final tax, it’s adjustable against your total liability at ITR filing time, with a refund (plus interest) due if you’ve overpaid.

How Form 15H Can Help You Avoid TDS

Senior citizens whose final tax liability works out to zero can file Form 15H to stop TDS at source. It needs to be submitted fresh every financial year. The form is based on your final tax liability after exemptions and rebates, so a senior citizen earning up to ₹12 lakh under the new regime could still have zero tax liability and qualify, per Chartered Accountant Suresh Surana.

Section 87A Rebate: What Applies For FY 2026-27

| Regime | Tax-Free Income Limit | Max Rebate |

|---|---|---|

| New Tax Regime | Up to ₹12 lakh (₹12.75 lakh with standard deduction for salaried) | ₹60,000 |

| Old Tax Regime (senior citizens, 60–79 yrs) | Up to ₹5 lakh | ₹12,500 |

| Old Tax Regime (super senior, 80+ yrs) | Up to ₹5 lakh | ₹12,500 |

These FY 2026-27 thresholds carry forward unchanged from Budget 2025. The rebate doesn’t apply to special-rate income such as capital gains on listed equity, even if total income stays under ₹12 lakh.

Bottom Line

The rate gap between bank categories is wide enough to matter: small finance banks offer up to 100 basis points more than PSU banks, and 140 basis points more than the best foreign bank rate.

But chasing the absolute top rate at a single small finance bank means running into the ₹5 lakh DICGC ceiling fast.

For most senior citizens, the practical approach is a mix, some allocation to the highest-paying SFBs, the rest spread across PSU or larger private banks for stability, with deposits sized to stay within insurance cover at each one. Tax-wise, FY 2026-27 brings no changes from last year, so Form 15H filers can continue the same routine.

Read Next: Max Pain in Options Explained: What It Predicts at Expiry and How Traders Use It

FAQs

Is FD interest fully tax-free for senior citizens?

No. FD interest is taxable as per your income slab. Form 15H only stops TDS at source if your final tax liability is nil, it doesn’t exempt the income itself.

What happens if I don’t submit Form 15H and my income is below the taxable limit?

The bank will still deduct TDS since it isn’t aware of your overall tax position. You can claim it back as a refund when you file your ITR.

Are small finance bank FDs as safe as those from large banks?

Small finance banks are RBI-licensed scheduled banks, and deposits are DICGC-insured up to ₹5 lakh, same as any other bank. The insurance cap, not the type of bank, is what limits your safety net.

Does the Section 87A rebate apply to FD interest?

Yes, FD interest is treated as normal income, so it counts toward your ₹12 lakh (new regime) or ₹5 lakh (old regime) threshold for the rebate.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. FD rates are subject to change at the bank’s discretion; verify current rates directly with the bank before investing. Please consult a SEBI-registered financial advisor before making investment decisions.